Technical Summary

This Technical Summary should be cited as:

M. Pathak, R. Slade, P.R. Shukla, J. Skea, R. Pichs-Madruga, D. Ürge-Vorsatz,2022: Technical Summary. In: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change[P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA. doi: 10.1017/9781009157926.002.

TS.1 Introduction

The Working Group III (WGIII) contribution to the IPCC’s Sixth Assessment Report (AR6) assesses the current state of knowledge on the scientific, technological, environmental, economic and social aspects of climate change mitigation. It builds on previous IPCC reports, including the WGIII contribution to the IPCC’s Fifth Assessment Report (AR5) and the three Special Reports of the Sixth Assessment cycle on: Global Warming of 1.5°C (SR1.5); Climate Change and Land (SRCCL); and the Ocean and Cryosphere in a Changing Climate (SROCC). 1

The report assesses new literature, methodological and recent developments, and changes in approaches towards climate change mitigation since the IPCC AR5 report was published in 2014.

The global science and policy landscape on climate change mitigation has evolved since AR5. The development of the literature reflects, among other factors, the UN Framework Convention on Climate Change (UNFCCC), the outcomes of its Kyoto Protocol and the goals of the Paris Agreement {13, 14, 15}, and the UN 2030 Agenda for Sustainable Development {1, 4, 17}. Literature further highlights the growing role of non-state and sub-national actors in the global effort to address climate change, including cities, businesses, citizens, transnational initiatives and public-private entities {5, 8, 13}. It draws attention to the decreasing cost of some low-emission technologies {2, 6, 12} and the evolving role of international cooperation {14}, finance {15} and innovation {16}. Emerging literature examines the global spread of climate policies, strengthened mitigation actions in developing countries, sustained reductions in greenhouse gas (GHG) emissions in some developed countries and the continuing challenges for mitigation. {2, 13}

There are ever closer linkages between climate change mitigation, development pathways and the pursuit of Sustainable Development Goals (SDGs). Development pathways largely drive GHG emissions and hence shape the mitigation challenge and the portfolio of available responses {4}. The co-benefits and risks of mitigation responses also differ according to stages of development and national capabilities {1, 2, 3, 4, 13}. Climate change mitigation framed in the context of sustainable development, equity, and poverty eradication, and rooted in the development aspirations of the society within which they take place, will be more acceptable, durable and effective. {1, 4, 17}

This report includes new assessment approaches that go beyond those evaluated in the previous IPCC WGIII reports. In addition to sectoral and systems chapters {6, 7, 8, 9, 10, 11}, this report includes, for the first time, chapters dedicated to cross-sectoral perspectives {12}, demand, services and social aspects of mitigation (Box TS.11) {5}, and innovation, technology development and transfer {16}. The assessment of future pathways combines a forward-looking assessment of near- to medium-term perspectives up to 2050, including ways of shifting development pathways towards sustainability {4}, with an assessment of long-term outcome-oriented pathways up to 2100 {3}. Collaboration between the IPCC Working Groups is reflected in Cross-Working Group boxes which address topics such as the economic benefits from avoided impacts along mitigation pathways {Cross-Working Group Box 1 in Chapter 3}, climate change and urban areas {Cross-Working Group Box 2 in Chapter 8}, mitigation and adaptation through the bioeconomy {Cross-Working Group Box 3 in Chapter 12} and Solar Radiation Modification (SRM) {Cross-Working Group Box 4 in Chapter 14}. This assessment also gives greater attention than AR5 to social, economic and environmental dimensions of mitigation actions, and institutional, legal and financial aspects. {5, 13, 14, 15}

The report draws from literature on broad and diverse analytic frameworks across multiple disciplines. These include, inter alia: economic and environmental efficiency {1}; ethics and equity {4, 5, 17}; innovation and the dynamics of socio-technical transitions {16}; and socio-political-institutional frameworks {1, 5, 13, 14, 17}. These help to identify synergies and trade-offs with Sustainable Development Goals (SDGs), challenges and windows of opportunity for action including co-benefits, and equitable transitions at local, national and global scales. {1, 5, 13, 14, 16}

This Technical Summary (TS) of the WGIII contribution to the IPCC’s Sixth Assessment Report (AR6) broadly follows the report chapter order and is structured as follows.

TS Section 2 (TS.2) sets out how the global context for mitigation has changed and summarises signs of progress and continuing challenges.

TS Section 3 (TS.3) evaluates emission trends and drivers including recent sectoral, financial, technological and policy developments.

TS Section 4 (TS.4) identifies mitigation and development pathways in the near and mid-term to 2050, and in the longer term to 2100. This section includes an assessment of how mitigation pathways deploying different portfolios of mitigation responses are consistent with limiting global warming to different levels.

TS Section 5 (TS.5) summarises recent advances in knowledge across sectors and systems including energy, urban and other settlements, transport, buildings, industry, and agriculture, forestry and other land-use (AFOLU).

TS Section 6 (TS.6) examines how enabling conditions including behaviour and lifestyle, policy, governance and institutional capacity, international cooperation, finance, and innovation and technology can accelerate mitigation in the context of sustainable development.

TS Section 7 (TS.7) evaluates how mitigation can be achieved in the context of sustainable development, while maximising co-benefits and minimising risks.

Throughout this Technical Summary the validity of findings, confidence in findings, and cross-references to Technical Summary sections, figures and tables are shown in ( ) brackets. 2 References to the underlying report are shown in { } brackets.

TS.2 The Changed Global Context, Signs of Progress and Continuing Challenges

Since the IPCC’s Fifth Assessment Report (AR5), important changes that have emerged include the specific objectives established in the Paris Agreement of 2015 (for temperature, adaptation and finance), rising climate impacts, and higher levels of societal awareness and support for climate action (high confidence). Meeting the long-term temperature goal in the Paris Agreement, however, implies a rapid inflection in GHG emission trends and accelerating decline towards ‘net zero’. This is implausible without urgent and ambitious action at all scales. {1.2, 1.3, 1.5, 1.6, Chapters 3 and 4}

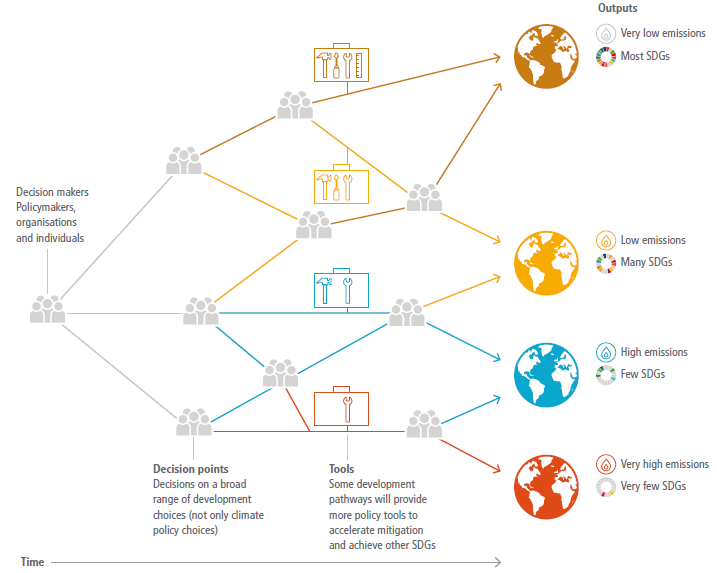

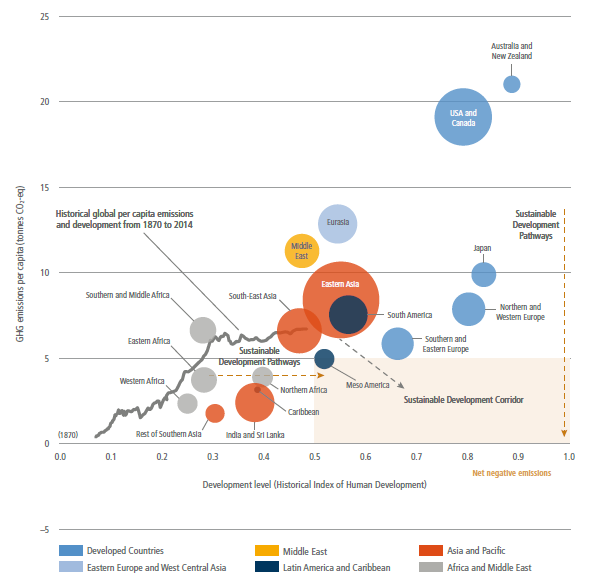

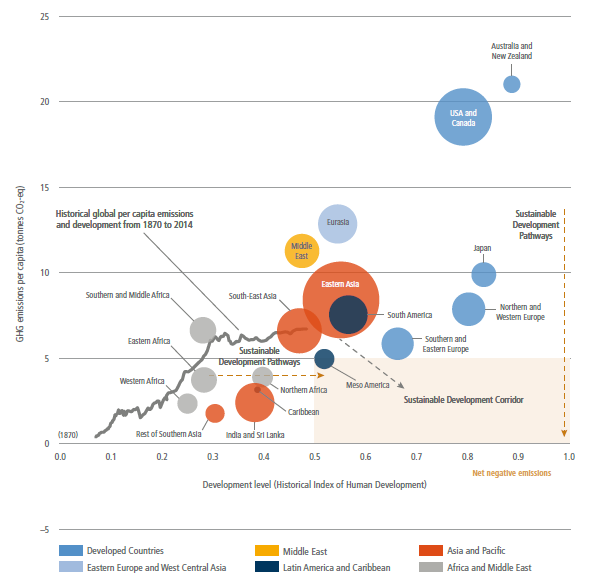

Effective and equitable climate policies are largely compatible with the broader goal of sustainable development and efforts to eradicate poverty as enshrined in the UN 2030 Agenda for Sustainable Development and its 17 Sustainable Development Goals (SDGs), notwithstanding trade-offs in some cases (high confidence). Taking urgent action to combat climate change and its impacts is one of the 17 SDGs (SDG 13). However, climate change mitigation also has synergies and/or trade-offs with many other SDGs. There has been a strong relationship between development and GHG emissions, as historically both per-capita and absolute emissions have risen with industrialisation. However, recent evidence shows countries can grow their economies while reducing emissions. Countries have different priorities in achieving the SDGs and reducing emissions as informed by their respective national conditions and capabilities. Given the differences in GHG emissions contributions, degree of vulnerability and impacts, as well as capacities within and between nations, equity and justice are important considerations for effective climate policy and for securing national and international support for deep decarbonisation. Achieving sustainable development and eradicating poverty would involve effective and equitable climate policies at all levels from local to global scale. Failure to address questions of equity and justice over time can undermine social cohesion and stability. International cooperation can enhance efforts to achieve ambitious global climate mitigation in the context of sustainable development. Pathways that illustrate movement towards fulfilling the SDGs are shown in Figure TS.1. {1.4, 1.6, Chapters 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 13 and 17}

Figure TS.1 | Sustainable development pathways towards fulfilling the Sustainable Development Goals. The graph shows global average per-capita GHG emissions (vertical axis) and relative ‘Historic Index of Human Development’ (HIHD) levels (horizonal) have increased globally since the industrial revolution (grey line). The bubbles on the graph show regional per-capita GHG emissions and human development levels in the year 2015, illustrating large disparities. Pathways towards fulfilling the Paris Agreement (and SDG 13) involve global average per-capita GHG emissions below about 5 tCO2-eq by 2030. Likewise, to fulfil SDGs 3, 4 and 8, HIHD levels (see footnote 7 in Chapter 1) need to be at least 0.5 or greater. This suggests a ‘sustainable development zone’ for year 2030 (in pale brown); the in-figure text also suggests a ‘sustainable development corridor’, where countries limit per-capita GHG emissions while improving levels of human development over time. The emphasis of pathways into the sustainable development zone differ (dashed brown arrows), but in each case transformations are needed in how human development is attained while limiting GHG emissions.

The transition to a low-carbon economy depends on a wide range of closely intertwined drivers and constraints, including policies and technologies where notable advances over the past decade have opened up new and large-scale opportunities for deep decarbonisation, and for alternative development pathways which could deliver multiple social and developmental goals (high confidence). Drivers for, and constraints on, low-carbon societal transitions comprise economic and technological factors (the means by which services such as food, heating and shelter are provided and for whom, the emissions intensity of traded products, finance and investment), socio-political issues (political economy, equity and fairness, social innovation and behaviour change), and institutional factors (legal framework and institutions, and the quality of international cooperation). In addition to being deeply intertwined, all the factors matter to varying degrees, depending on the prevailing social, economic, cultural and political context. They often both drive and inhibit transitions at the same time, within and across different scales. The development and deployment of innovative technologies and systems at scale are important for achieving deep decarbonisation, and in recent years, the cost of several low-carbon technologies has declined sharply as deployment has risen rapidly. (Figure TS.7) {1.3, 1.4, Chapters 2, 4, 5, 13,14}

Accelerating mitigation to prevent dangerous anthropogenic interference with the climate system will require the integration of broadened assessment frameworks and tools that combine multiple perspectives, applied in a context of multi-level governance (high confidence). Analysing a challenge on the scale of fully decarbonising our economies entails integration of multiple analytic frameworks. Approaches to risk assessment and resilience, established across IPCC Working Groups, are complemented by frameworks for probing the challenges in implementing mitigation. Aggregate frameworks include cost-effectiveness analysis towards given objectives, and cost-benefit analysis, both of which have been developing to take fuller account of advances in understanding risks and innovation, the dynamics of sectors and systems and of climate impacts, and welfare economic theory including growing consensus on long-term discounting. Ethical frameworks consider the fairness of processes and outcomes which can help ameliorate distributional impacts across income groups, countries and generations. Transition and transformation frameworks explain and evaluate the dynamics of transitions to low-carbon systems arising from interactions amongst levels. Psychological, behavioural and political frameworks outline the constraints (and opportunities) arising from human psychology and the power of incumbent interests. A comprehensive understanding of climate mitigation must combine these multiple frameworks. Together with established risk frameworks, these collectively help to explain potential synergies and trade-offs in mitigation, implying a need for a wide portfolio of policies attuned to different actors and levels of decision-making, and underpin ‘just transition’ strategies in diverse contexts. {1.2.2, 1.7, 1.8, Figure 1.7}

The speed, direction, and depth of any transition will be determined by choices in the environmental, technological, economic, socio-cultural and institutional realms (high confidence). Transitions in specific systems can be gradual or can be rapid and disruptive. The pace of a transition can be impeded by ‘lock-in’ generated by existing physical capital, institutions, and social norms. The interaction between politics, economics and power relationships is central to explaining why broad commitments do not always translate to urgent action. At the same time, attention to, and support for, climate policies and low-carbon societal transitions has generally increased, as the impacts have become more salient. Both public and private financing and financial structures strongly affect the scale and balance of high- and low-carbon investments. Societal and behavioural norms, regulations and institutions are essential conditions to accelerate low-carbon transitions in multiple sectors, whilst addressing distributional concerns endemic to any major transition. The COVID-19 pandemic has also had far-reaching impacts on the global economic and social system, and recovery will present both challenges and opportunities for climate mitigation. (Box TS.1) {1.3, Box 1.1, 1.4, 1.8, Chapters 2, 3, 4, 5, 15, 17}

Achieving the global transition to a low-carbon, climate-resilient and sustainable world requires purposeful and increasingly coordinated planning and decisions at many scales of governance including local, sub-national, national and global levels (high confidence). Accelerating mitigation globally would imply strengthening policies adopted to date, expanding the effort across options, sectors, and countries, and broadening responses to include more diverse actors and societal processes at multiple – including international – levels. The effective governance of climate change entails strong action across multiple jurisdictions and decision-making levels, including regular evaluation and learning. Choices that cause climate change as well as the processes for making and implementing relevant decisions involve a range of non-nation state actors such as cities, businesses, and civil society organisations. At global, national and sub-national levels, climate change actions are interwoven with, and embedded in, the context of much broader social, economic and political goals. Therefore, the governance required to address climate change has to navigate power, political, economic, and social dynamics at all levels of decision-making. Effective climate-governing institutions, and openness to experimentation on a variety of institutional arrangements, policies and programmes can play a vital role in engaging stakeholders and building momentum for effective climate action. {1.4, 1.9, Chapters 8, 13, 15, 17}

Table TS.1 | Signs of progress and continuing challenges.

Signs of progress | Continuing challenges |

Emissions trends | |

The rate of global GHG emissions growth has slowed in recent years, from 2.1% yr –1 between 2000 and 2009, to 1.3% yr –1 in between 2010 and 2019. (TS.3) {2.2} | GHG emissions have continued to grow at high absolute rates. Emissions increased by 8.9 GtCO2-eq from 2000 to 2009 and by 6.5 GtCO2-eq from 2010 to 2019, reaching 59 GtCO2-eq in 2019. (TS.3) {2.2} |

A growing number of countries have reduced both territorial carbon dioxide (CO2) and GHG emissions and consumption-based CO2 emissionsin absolute terms for at least 10 years. These include mainly European countries, some of which have reduced production-based GHG emissions by a third or more since peaking. Some countries have achieved several years of rapid sustained CO2 reduction rates of 4% yr –1. (TS.3) {2.2} | The combined emissions reductions achieved by some countries have been outweighed by rapid emissions growth elsewhere, particularly among developing countries that have grown from a much lower base of per-capita emissions. Uncertainties in emissions levels and changes over time prevents a precise assessment of reductions in some cases. The per-capita emissions of developed countries remain high, particularly in Australia, Canada, and the United States of America. {2.2} |

Lockdown policies in response to COVID-19 led to an estimated global drop of 5.8% in CO2 emissions in 2020 relative to 2019. Energy demand reduction occurred across sectors, except in residential buildings due to teleworking and homeschooling. The transport sector was particularly impacted and international aviation emissions declined by 45%. (Box TS.1) {2.2} | Atmospheric CO2concentrations continued to rise in 2020 and emissions have already rebounded as lockdown policies are eased. Economic recovery packages currently include support for fossil fuel industries. (Boxes TS.1 and TS.8) |

Sectors | |

Multiple low-carbon electricity generation and storage technologies have made rapid progress: costs have reduced, deployment has scaled up, and performance has improved. These include solar photovoltaics (PV), onshore and offshore wind, and batteries. In many contexts solar PV and onshore wind power are now competitive with fossil-based generation. (TS.3) {2.5, 6.3} | Although deployment is increasing rapidly, low-carbon electricity generation deployment levels and rates are currently insufficient to meet stringent climate goals. The combined market share of solar PV and wind generation technologies are still below 10%. Global low-carbon electricity generation will have to reach 100% by 2050, which is challenged by the continuous global increase in electricity demand. The contribution of biomass has absolute limits. (TS.5) {2.5} |

The rate of emissions growth from coal slowed since 2010 as coal power plants were retired in the US and Europe, fewer new plants were added in China, and a large number of planned global plants were scrapped or converted to co-firing with biomass. (TS.3) {2.7, 6.3} | Global coal emissions may not have peaked yet, and a few countries and international development banks continue to fund and develop new coal capacity, especially abroad. The lifetime emissions of current fossil-based energy infrastructures may already exceed the remaining carbon budget for keeping warming below 1.5°C. (TS.3) {2.2, 2.7, 6.7} |

Deforestation has declined since 2010 and net forest cover increased. Government initiatives and international moratoria were successful in reducing deforestation in the Amazon between 2004 and 2015, while regrowth and regeneration occurred in Europe, Eurasia and North America. (TS.5.6.1) {7.3.1} | The long-term maintenance of low deforestation rates is challenging. Deforestation in the Amazon has risen again over the past four years. Other parts of the world also face steady, or rapidly increasing, deforestation. {7.3.1} |

Electrification of public transport services is demonstrated as a feasible, scalable and affordable mitigation option to decarbonise mass transportation. Electric vehicles (e-vehicles) are the fastest growing segment of the automobile industry, having achieved double-digit market share by 2020 in many countries. When charged with low-carbon electricity, these vehicles can significantly reduce emissions. {10.4} | Transport emissions have remained roughly constant, growing at an average of 2% yr–1between 2010 and 2019 due to the persistence of high travel demand, heavier vehicles, low efficiencies, and car-centric development. The full decarbonisation of e-vehicles requires that they are charged with zero-carbon electricity, and that car production, shipping, aviation and supply chains are decarbonised. (TS.3) {2.4} |

There has been a significant global transition from coal and biomass use in buildings towards modern energy carriers andefficient conversiontechnologies. This led to efficiency improvements and some emissions reductions in developed countries, as well as significant gains in health and well-being outcomes in developing regions. Nearly zero energy buildings (nZEB) or low-energy buildings are achievable in all regions and climate zones for both new and existing buildings. {9.3, 9.8} | There is a significant lock-in risk in all regions given the long lifespansof buildings and the low ambition of building policies. This is the case for both existing buildings in developed countries, and also for new buildings in developing countries that are also challenged by the lack of technical capacity and effective governance. Emissions reductions in developed countries have been outweighed by the increase in population growth, floor area per capita and the demand for electricity and heat. {9.3, 9.9} |

The decarbonisation of most industrial processes has been demonstrated using technologies that include electricity and hydrogen for energy and feedstocks, carbon capture and utilisation technologies, and innovation in circular material flows. (TS.5.5) {11.2} | Industry emissions continue to increase, driven by a strong global demand for basic materials. Without reductions in material demand growth and a very rapid scale-up of low-carbon innovations, the long lifetimes of industrial capital stock risks locking-in emissions for decades to come. (TS.5.5) {11.2} |

Policies and investment | |

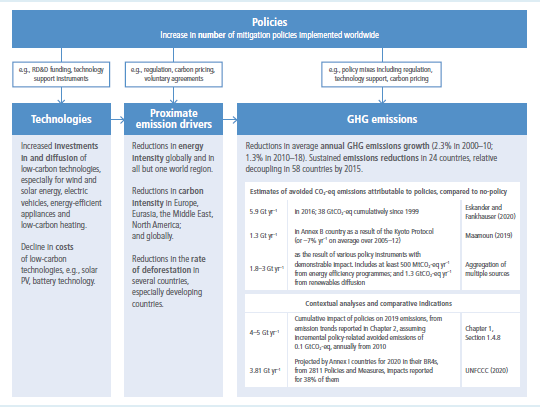

The Paris Agreement established a new global policy architecture to meet stringent climate goals, while avoiding many areas of deadlock that had arisen in trying to extend the Kyoto Protocol. (TS.6.3) | Current national pledges under the Paris Agreement 3 are insufficient tolimit warming to 1.5°C (>50%) with no or limited overshoot, and would requirean abrupt acceleration of mitigation efforts after 2030 to limit warming to 2°C (>67%). (TS.6.3) |

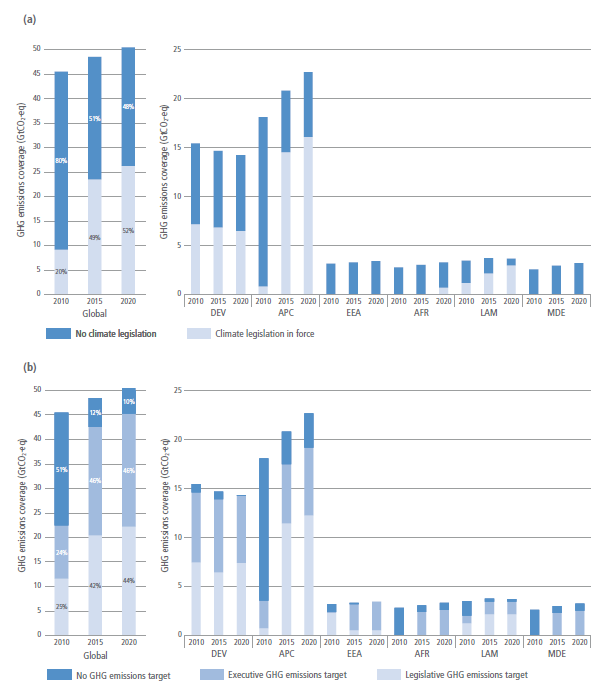

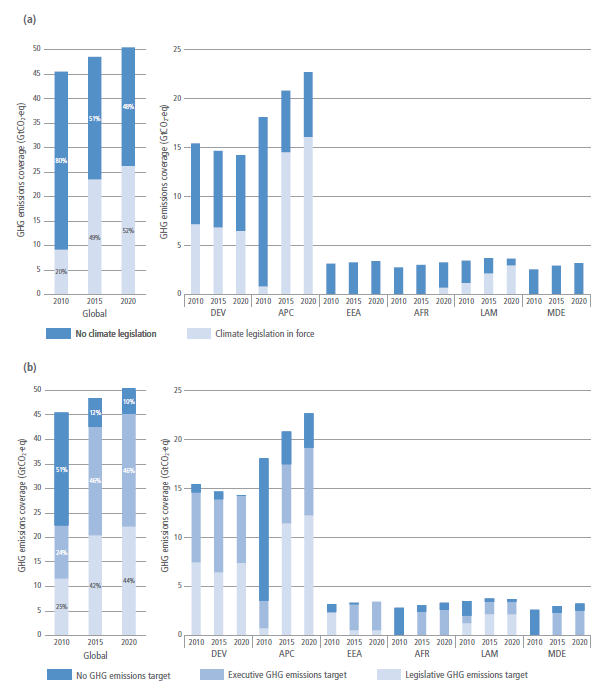

Most wealthy countries, and a growing list of developing countries, have signalled an intention to achieve net zero GHG (or net zero CO2) emissions by mid-century. National economy-wide GHG emissions targets covered 90% of global emissions in 2020 compared to 49% in 2010. Direct and indirect climate legislation has also steadily increased and this is supported by a growing list of financial investors. (TS.6.2) | Many net-zero targets are ambiguously defined, and the policies needed to achieve them are not yet in place. Opposition from status quo interests, as well as insufficient low-carbon financial flows, act as barriers to establishing and implementing stringent climate policies covering all sectors. (Box TS.6) {13.4} |

The global coverage of mandatory policies – pricing and regulation – has increased, and sectoral coverage of mitigation policies has expanded. Emission trading and carbon taxes now cover over 20% of global CO2 emissions. Allowance prices as of 1 April 2021 ranged from just over USD1 to USD50, covering between 9% and 80% of a jurisdiction’s emissions {13.6.3}. Many countries have introduced sectoral regulations that block new investment in fossil fuel technologies. (TS.6) | There is incomplete global policy coverage of non-CO2gases, CO2from industrial processes, and emissions outside the energy sector. Few of the world’s carbon prices are at a level consistent with various estimates of the carbon price needed to limit warming to 2°C or 1.5°C. {13.6} |

There has been a marked increase in civic and private engagement with climate governance. This includes business measures to limit emissions, invest in reforestation and develop carbon-neutral value chains such as using wood for construction. There is an upsurge in climate activism, and growing engagement of groups such as labour unions {1.3.3, 5.2.3}. The media coverage of climate change has also grown steadily across platforms and has generally become more accurate over time. (TS.6.2) | There is no conclusive evidence that an increase in engagement results in overall pro-mitigation outcomes. A broad group of actors influence how climate governance develops over time, including a range of civic organisations, encompassing both pro-and anti-climate action groups. Accurate transference of the climate science has been undermined significantly by climate change counter-movements, in both legacy and new/social media environments through misinformation. (TS.6.2) |

GHG emissions continued to rise to 2019, although the growth of global GHG emissions has slowed over the past decade (high confidence). Delivering the updated Nationally Determined Contributions (NDCs) to 2030 would turn this into decline, but the implied global emissions by 2030, still exceed pathways consistent with 1.5°C by a large margin and are near the upper end of the range of modelled pathways that limit warming to 2°C (>67%) or below. In all chapters of this report there is evidence of progress towards deeper mitigation, but there remain many obstacles to be overcome. Table TS.1 summarises some of the key signs of progress in emission trends, sectors, policies and investment, as well as the challenges that persist.

TS.3 Emission Trends and Drivers

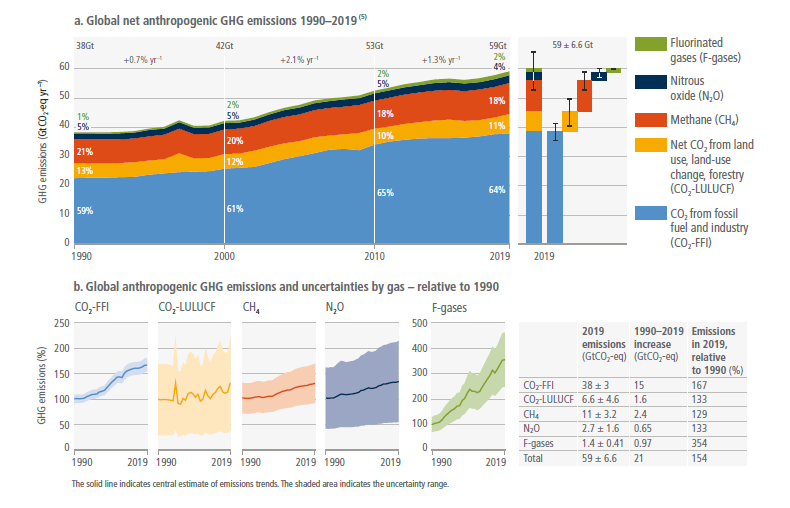

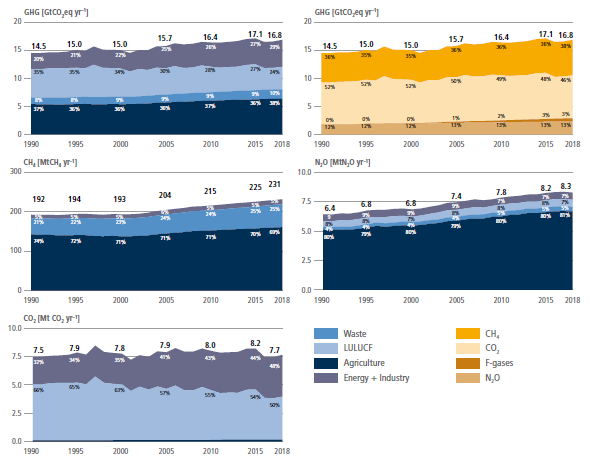

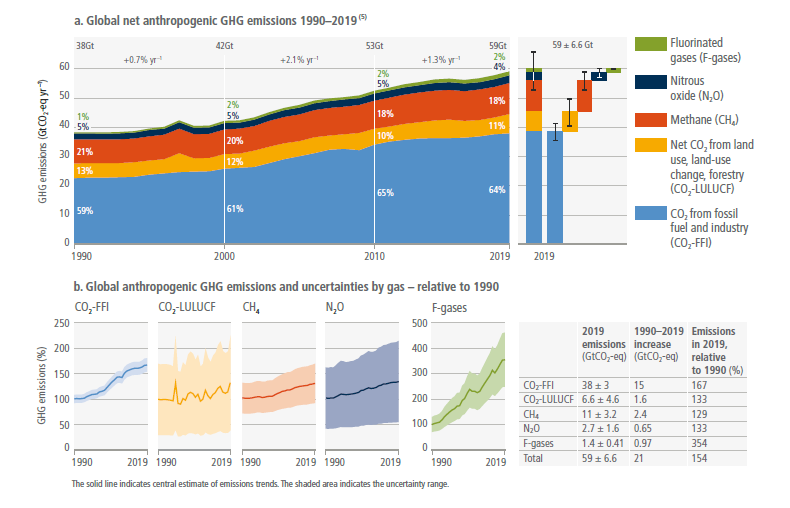

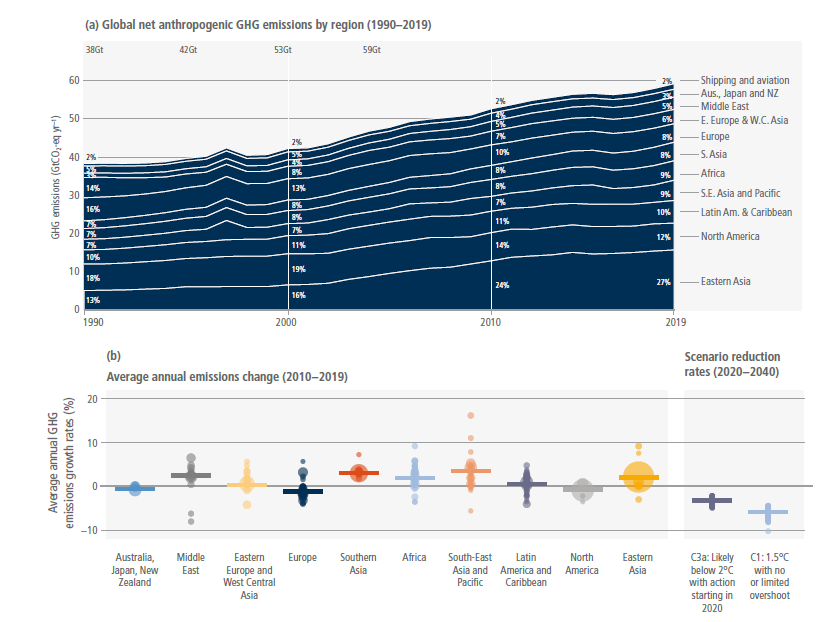

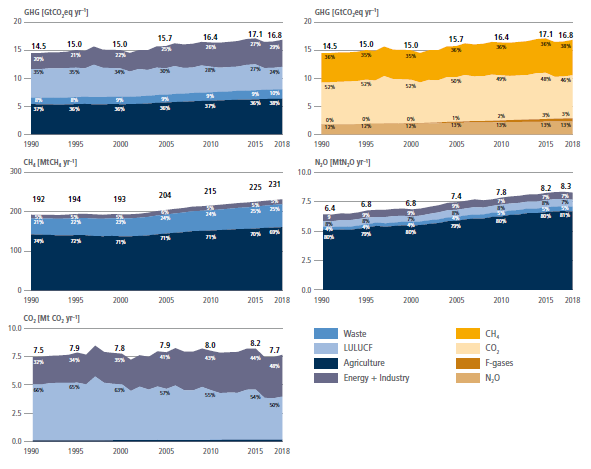

Global net anthropogenic GHG emissions during the decade 2010–2019 were higher than any previous time in human history (high confidence). Since 2010, GHG emissions have continued to grow reaching 59 ± 6.6 GtCO2-eq in 2019, 4 but the average annual growth in the last decade (1.3%, 2010–2019) was lower than in the previous decade (2.1%, 2000–2009) ( high confidence). Average annual GHG emissions were 56 GtCO2-eq yr –1 for 2010–2019 (the highest decadal average on record) growing by about 9.1 GtCO2-eq yr –1 from the previous decade (2000–2009) ( high confidence). (Figure TS.2) {2.2.2, Table 2.1, Figure 2.5}

Emissions growth has varied, but has persisted, across all groups of greenhouse gases (high confidence). The average annual emission levels of the last decade (2010–2019) were higher than in any previous decade for each group of greenhouse gases ( high confidence). In 2019, CO2 emissions were 45 ± 5.5 GtCO2, 5 methane (CH4) 11 ± 3.2 GtCO2-eq, nitrous oxide (N2O) 2.7 ± 1.6 GtCO2-eq and fluorinated gases (F-gases 6 ) 1.4 ± 0.41 GtCO2-eq. Compared to 1990, the magnitude and speed of these increases differed across gases: CO2 from fossil fuel and industry (FFI) grew by 15 GtCO2-eq yr –1 (67%), CH4 by 2.4 GtCO2-eq yr –1 (29%), F-gases by 0.97 GtCO2-eq yr –1 (250%), N2O by 0.65 GtCO2-eq yr –1 (33%). CO2 emissions from net land use, land-use change and forestry (LULUCF) have shown little long-term change, with large uncertainties preventing the detection of statistically significant trends. F-gases excluded from GHG emissions inventories such as chlorofluorocarbons and hydrochlorofluorocarbons are about the same size as those included ( high confidence). (Figure TS.2) {2.2.1, 2.2.2, Table 2.1, Figures 2.2, 2.3 and 2.5}

Figure TS.2 | Global net anthropogenic GHG emissions (GtCO2-eqyr–1) 1990–2019. Global net anthropogenic GHG emissions include CO2 from fossil fuel combustion and industrial processes (CO2-FFI); net CO2 from land use, land-use change and forestry (CO2-LULUCF)5; methane (CH4); nitrous oxide (N2O); and fluorinated gases (HFCs, PFCs, SF6, NF3). 6Panel a shows aggregate annual global net anthropogenic GHG emissions by groups of gases from 1990 to 2019 reported in GtCO2-eq converted based on global warming potentials with a 100-year time horizon (GWP100-AR6) from the IPCC Sixth Assessment Report Working Group I (Chapter 7). The fraction of global emissions for each gas is shown for 1990, 2000, 2010 and 2019; as well as the aggregate average annual growth rate between these decades. At the right side of Panel a, GHG emissions in 2019 are broken down into individual components with the associated uncertainties (90% confidence interval) indicated by the error bars: CO2-FFI ±8%; CO2-LULUCF ±70%; CH4±30%; N2O ±60%; F-gases ±30%; GHG ±11%. Uncertainties in GHG emissions are assessed in Supplementary Material 2.2. The single-year peak of emissions in 1997 was due to higher CO2-LULUCF emissions from a forest and peat fire event in South East Asia. Panel b shows global anthropogenic CO2-FFI, net CO2-LULUCF, CH4, N2O and F-gas emissions individually for the period 1990–2019, normalised relative to 100 in 1990. Note the different scale for the included F-gas emissions compared to other gases, highlighting its rapid growth from a low base. Shaded areas indicate the uncertainty range. Uncertainty ranges as shown here are specific for individual groups of greenhouse gases and cannot be compared. The table shows the central estimate for: absolute emissions in 2019; the absolute change in emissions between 1990 and 2019; and emissions in 2019 expressed as a percentage of 1990 emissions. {2.2, Figure 2.5, Supplementary Material 2.2, Figure TS.2}

Globally, gross domestic product (GDP) per capita and population growth remained the strongest drivers of CO2 emissions from fossil fuel combustion in the last decade (high confidence). Trends since 1990 continued in the years 2010 to 2019 with GDP per capita and population growth increasing emissions by 2.3% yr –1 and 1.2% yr –1, respectively. This growth outpaced the reduction in the use of energy per unit of GDP (–2% yr –1, globally) as well as improvements in the carbon intensity of energy (–0.3% yr –1). {2.4.1, Figure 2.19}

Box TS.1 | The COVID-19 Pandemic: Impact on Emissions and Opportunities for Mitigation

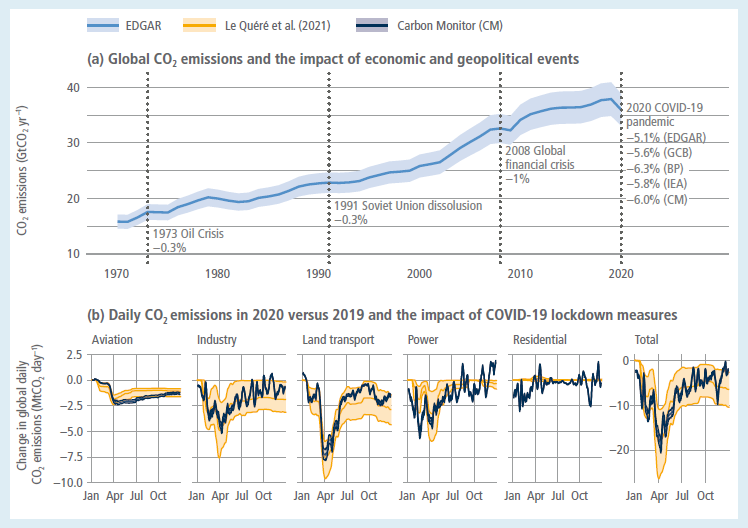

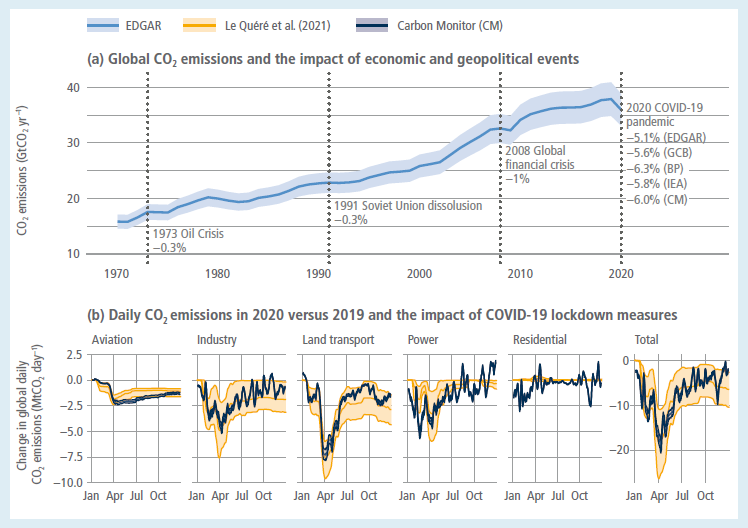

The COVID-19 pandemic triggered the deepest global economic contraction as well as CO2 emission reductions since the Second World War {2.2.2}. While emissions and most economies rebounded in 2020, some impacts of the pandemic could last well beyond this. Owing to the very recent nature of this event, it remains unclear what the exact short- and long-term impacts on global emissions drivers, trends, macroeconomics and finance will be.

Starting in the spring of 2020 a major break in global emissions trends was observed due to lockdown policies implemented in response to the pandemic. Overall, global CO2-FFI emissions are estimated to have declined by 5.8% (5.1–6.3%) in 2020, or about 2.2 (1.9–2.4%) GtCO2 in total. This exceeds any previous global emissions decline since 1970 both in relative and absolute terms (Box TS.1, Figure 1). During periods of economic lockdown, daily emissions, estimated based on activity and power-generation data, declined substantially compared to 2019, particularly in April 2020 – as shown in Box TS.1, Figure 1 – but rebounded by the end of 2020. Impacts were differentiated by sector, with road transport and aviation particularly affected. Different databases estimate the total power-sector CO2 reduction from 2019 to 2020 at 3% (IEA7 ) and 4.5% (EDGAR8 ). Approaches that predict near real-time estimates of the power-sector reduction are more uncertain and estimates range more widely between 1.8%, 4.1% and 6.8%, the latter taking into account the over-proportional reduction of coal generation due to low gas prices and merit order effects.

Box TS.1, Figure1 | Global carbon emissions in 2020 and the impact of COVID-19. Panel (a) depicts carbon emissions from fossil fuel and industry over the past five decades. The single-year declines in emissions following major economic and geopolitical events are shown, as well as the decline recorded in five different datasets for emissions in 2020 compared to 2019. Panel (b) depicts the perturbation of daily carbon emissions in 2020 compared to 2019, showing the impact of COVID-19 lockdown policies. {Figure 2.6}

The lockdowns implemented in many countries accelerated some specific trends, such as the uptake in urban cycling. The acceptability of collective social change over a longer term towards less resource-intensive lifestyles, however, depends on the social mandate for change. This mandate can be built through public participation, discussion and debate, to produce recommendations that inform policymaking. {Box 5.2}

Most countries were forced to undertake unprecedented levels of short-term public expenditures in 2021. This is expected to slow economic growth and may squeeze financial resources for mitigation and relevant investments in the near future. Pandemic responses have increased sovereign debt across countries in all income bands and the sharp increase in most developing economies and regions has caused debt distress, widening the gap in developing countries’ access to capital. {15.6.3}

The wider overall reduction in energy investment has prompted a relative shift towards low-carbon investment particularly for major future investment decisions by the private sector {15.2.1, 15.3.1, 15.6.1}. Some countries and regions have prioritised green stimulus expenditures, for example, as part of a ‘Green New Deal’ {Box 13.1}. This is motivated by assessments that investing in new growth industries can boost the macroeconomic effectiveness (‘multipliers’) of public spending, crowd-in and revive private investment, whilst also delivering on mitigation commitments. {15.2.3}

The impacts of COVID-19 may have temporarily set back development and the delivery of many SDGs. It also distracts political and financial capacity away from efforts to accelerate climate change mitigation and shift development pathways to increased sustainability. Yet, studies of previous post-shock periods suggest that waves of innovation that are ready to emerge can be accelerated by crises, which may prompt new behaviours, weaken incumbent systems, and initiate rapid reform. {1.6.5}

Institutional change can be slow but major economic dislocation can create significant opportunities for new ways of financing and enabling ‘leapfrogging’ investment {10.8}. Given the unambiguous risks of climate change, and consequent stranded asset risks from new fossil fuel investments {Box 6.11}, the most robust recoveries may well be those which align with lower carbon and resilient development pathways.

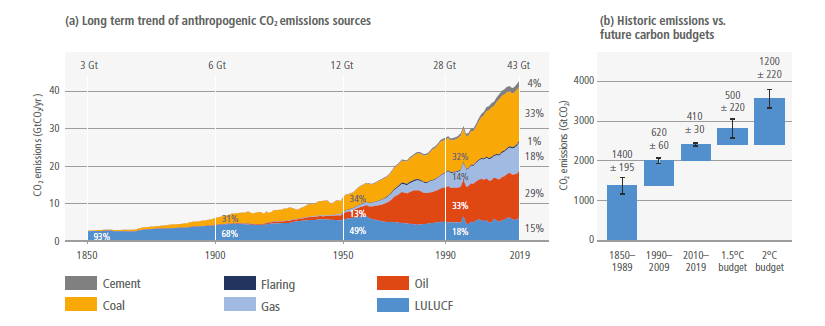

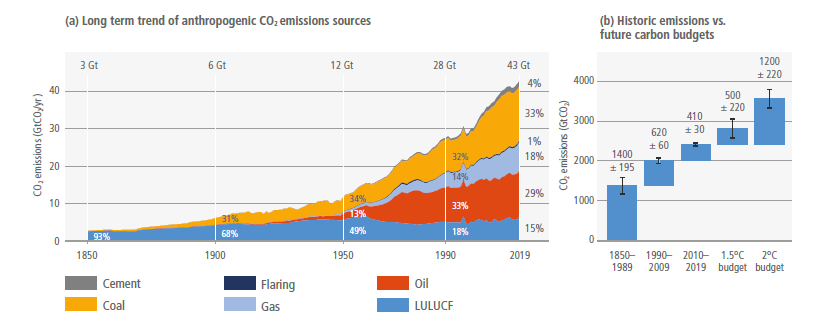

Cumulative net CO2 emissions over the last decade (2010–2019) are about the same size as the remaining carbon budget to limit warming to 1.5°C (>67%) (medium confidence). 62% of total cumulative CO2 emissions from 1850 to 2019 occurred since 1970 (1500 ± 140 GtCO2), about 43% since 1990 (1000 ± 90 GtCO2), and about 17% since 2010 (410 ± 30 GtCO2). For comparison, the remaining carbon budget for keeping warming to 1.5°C with a 67% (50%) probability is about 400 (500) ± 220 GtCO2 (Figure TS.3). {2.2.2, Figure 2.7, AR6 WGI Chapter 5.5, AR6 WGI Chapter 5, Table 5.8}

Figure TS. 3 | Historic anthropogenic CO2emission and cumulative CO2 emissions (1850–2019) as well as remaining carbon budgets for limiting warming to 1.5°C (>67%) and 2°C (>67%). Panel (a) shows historic annual anthropogenic CO2 emissions (GtCO2 yr –1) by fuel type and process. Panel (b) shows historic cumulative anthropogenic CO2 emissions for the periods 1850–1989, 1990–2009, and 2010–2019 as well as remaining future carbon budgets as of 1 January 2020 to limit warming to 1.5°C and 2°C at the 67th percentile of the transient climate response to cumulative CO2 emissions. The whiskers indicate a budget uncertainty of ±220 GtCO2-eq for each budget and the aggregate uncertainty range at one standard deviation for historical cumulative CO2 emissions, consistent with WGI. {Figure 2.7}

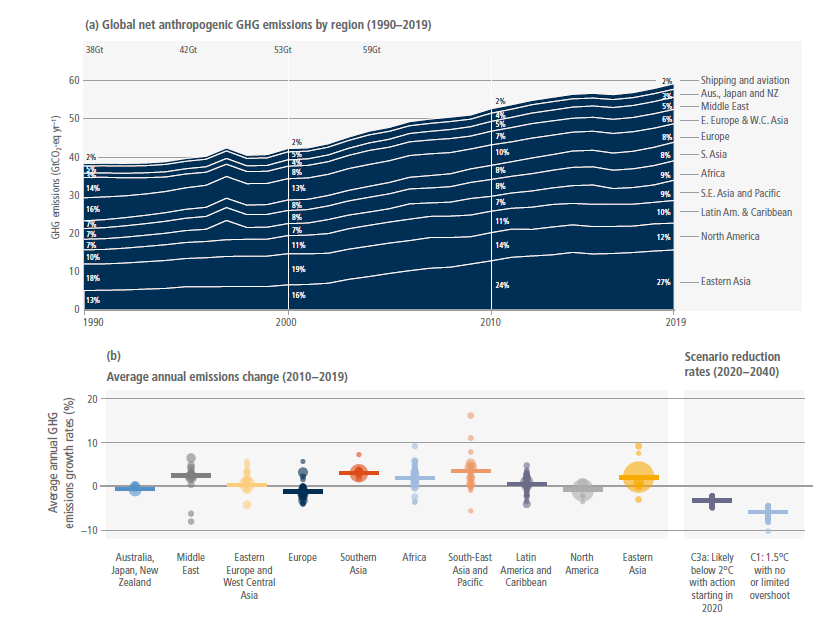

A growing number of countries have achieved GHG emission reductions over periods longer than 10 years – a few at rates that are broadly consistent with the global rates described in climate change mitigation scenarios that limit warming to 2°C (>67%) (high confidence). At least 18 countries have reduced CO2 and GHG emissions for longer than 10 years. Reduction rates in a few countries have reached 4% in some years, in line with global rates observed in pathways that limit warming to 2°C (>67%). However, the total reduction in annual GHG emissions of these countries is small (about 3.2 GtCO2-eq yr –1) compared to global emissions growth observed over the last decades. Complementary evidence suggests that countries have decoupled territorial CO2 emissions from GDP, but fewer have decoupled consumption-based emissions from GDP. Decoupling has mostly occurred in countries with high per-capita GDP and high per-capita CO2 emissions. (Figure TS.4, Box TS.2) {2.2.3, 2.3.3, Figure 2.11, Tables 2.3 and 2.4}

Figure TS.4 | Emissions have grown in most regions, although some countries have achieved sustained emission reductions in line with 2°C scenarios. Emissions have grown in most regions, although some countries have achieved sustained emission reductions in line with 2°C scenarios. Change in regional GHG emissions and rates of change compatible with warming targets. Panel (a): Regional GHG emission trends (in GtCO2-eq yr –1 (GWP100; AR6) for the time period 1990–2019. Panel (b): Historical GHG emissions change by region (2010–2019). Circles depict countries, scaled by total emissions in 2019, short horizontal lines depict the average change by region. Also shown are global rates of reduction over the period 2020–2040 in scenarios assessed in AR6 that limit global warming to 1.5°C and 2°C with different probabilities. The 5–95th percentile range of emissions changes for scenarios below 1.5°C with no or limited overshoot (scenario category C1) and scenarios below 2°C (>67%) with immediate action (scenario category C3a) are shown as a shaded area with a horizontal line at the mean value. Panel b excludes CO2LULUCF due to a lack of consistent historical national data, and International Shipping and Aviation, which cannot be allocated to regions. Global rates of reduction in scenarios are shown for illustrative purposes only and do not suggest rates of reduction at the regional or national level. {Figures 2.9 and 2.11}

Box TS.2 | Greenhouse Gas (GHG) Emission Metrics Provide Simplified Information About the Effects of Different Greenhouse Gases

Comprehensive mitigation policy relies on consideration of all anthropogenic forcing agents, which differ widely in their atmospheric lifetimes and impacts on the climate system. GHG emission metrics provide simplified information about the effect that emissions of different gases have on global temperature or other aspects of climate, usually expressed relative to the effect of emitting CO2. 9 This information can support choices about priorities, trade-offs and synergies in mitigation policies and emission targets for non-CO2 gases relative to CO2 as well as baskets of gases expressed in CO2-eq.

The choice of metric can affect the timing and emphasis placed on reducing emissions of short-lived climate forcers (SLCFs) relative to CO2 within multi-gas abatement strategies as well as the costs of such strategies. Different metric choices can also alter the time at which net zero GHG emissions are calculated to be reached for any given emissions scenario. A wide range of GHG emission metrics has been published in the scientific literature, which differ in terms of: (i) the key measure of climate change they consider, (ii) whether they consider climate outcomes for a specified point in time or integrated over a specified time horizon, (iii) the time horizon over which the metric is applied, (iv) whether they apply to a single emission pulse, to emissions sustained over a period of time, or to a combination of both, and (v) whether they consider the climate effect from an emission compared to the absence of that emission, or compared to a reference emissions level or climate state. {Annex II}

Parties to the Paris Agreement decided to report aggregated emissions and removals (expressed as CO2-eq) based on the Global Warming Potential (GWP) with a time horizon of 100 years (GWP100) using values from IPCC AR5 or from a subsequent IPCC report as agreed upon by the CMA, 10 and to account for future Nationally Determined Contributions (NDCs) in accordance with this approach. Parties may also report supplemental information on aggregate emissions and removals, expressed as CO2-eq, using other GHG emission metrics assessed by the IPCC.

The WGIII contribution to AR6 uses updated GWP100 values from AR6 WGI to report aggregate emissions and removals unless stated otherwise. These reflect updated scientific understanding of the response of the climate system to emissions of different gases and include a methodological update to incorporate climate-carbon cycle feedbacks associated with the emission of non-CO2 gases (see Annex II.II.8 for a list of GWP100 metric values). The choice of GWP100 was made inter alia for consistency with decisions under the Rulebook for the Paris Agreement and because it is the dominant metric used in the literature assessed by WGIII. Furthermore, for mitigation pathways that limit global warming to 2°C (>67%) or lower, using GWP100 to inform cost-effective abatement choices between gases would achieve such long-term temperature goals at close to least global cost within a few percent ( high confidence).

However, GWP100 is not well-suited to estimate the cumulative effect on climate from sustained SLCF emissions and the resulting warming at specific points in time. This is because the warming caused by an individual SLCF emission pulse is not permanent, and hence, unlike CO2, the warming from successive SLCF emission pulses over multiple decades or centuries depends mostly on their ongoing rate of emissions rather than cumulative emissions. Recently developed step/pulse metrics such as the CGTP (combined global temperature change potential) and GWP* (referred to as GWP-star and indicated by an asterisk) recognise that a sustained increase/decrease in the rate of SLCF emissions has indeed a similar effect on global surface temperature as one-off emission/removal of CO2. These metrics use this relationship to calculate the CO2 emissions or removals that would result in roughly the same temperature change as a sustained change in the rate of SLCF emissions (CGTP) over a given time period, or as a varying time series of CH4 emissions (GWP*). IFrom a mitigation perspective, this makes these metrics well-suited in principle to estimate the effect on the remaining carbon budget from more, or less, ambitious SLCF mitigation over multiple decades compared to a given reference scenario ( high confidence). However, potential application in wider climate policy (e.g., to inform equitable and ambitious emission targets or to support sector-specific mitigation policies) is contested and relevant literature still limited.

All metrics have limitations and uncertainties, given that they simplify the complexity of the physical climate system and its response to past and future GHG emissions. For this reason, the WGIII contribution to the AR6 reports emissions and mitigation options for individual gases where possible; CO2-equivalent emissions are reported in addition to individual gas emissions where this is judged to be policy-relevant. This approach aims to reduce the ambiguity regarding actual climate outcomes over time arising from the use of any specific GHG emission metric. {Cross-Chapter Box 2 in Chapter 2, SM.2.3, Annex II.II.8; AR6 WGI Chapter 7.6}

Consumption-based CO2 emissions in Developed Countries and the Asia and Pacific region are higher than in other regions (high confidence). In Developed Countries, consumption-based CO2 emissions peaked at 15 GtCO2 in 2007, declining to about 13 GtCO2 in 2018. The Asia and Developing Pacific region, with 52% of the current global population, has become a major contributor to consumption-based CO2 emission growth since 2000 (5.5% yr –1 for 2000–2018); in 2015 it exceeded the Developed Countries region, with 16% of global population, as the largest emitter of consumption-based CO2. {2.3.2, Figure 2.14}

Carbon-intensity improvements in the production of traded products has led to a net reduction in CO2 emissions embodied in international trade (high confidence). A decrease in the carbon intensity of traded products has offset increased trade volumes between 2006 and 2016. Emissions embodied in internationally traded products depend on the composition of the global supply chain across sectors and countries and the respective carbon intensity of production processes (emissions per unit of economic output). {2.3, 2.4}

Developed Countries tend to be net CO2emission importers, whereas developing countries tend to be net emission exporters (high confidence). Net CO2 emission transfers from developing to Developed Countries via global supply chains have decreased between 2006 and 2016. Between 2004 and 2011, CO2 emissions embodied in trade between developing countries have more than doubled (from 0.47 to 1.1 Gt) with the centre of trade activities shifting from Europe to Asia. {2.3.4, Figure 2.15}

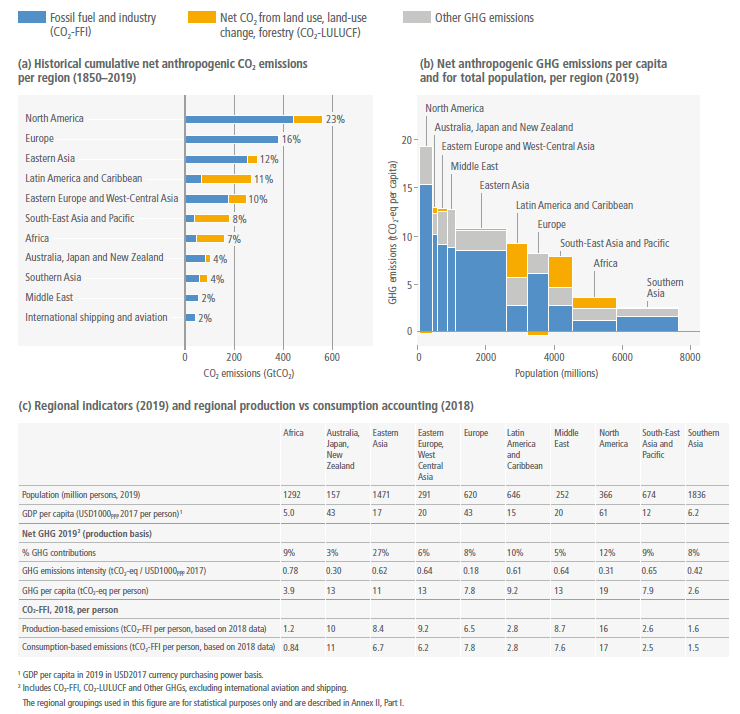

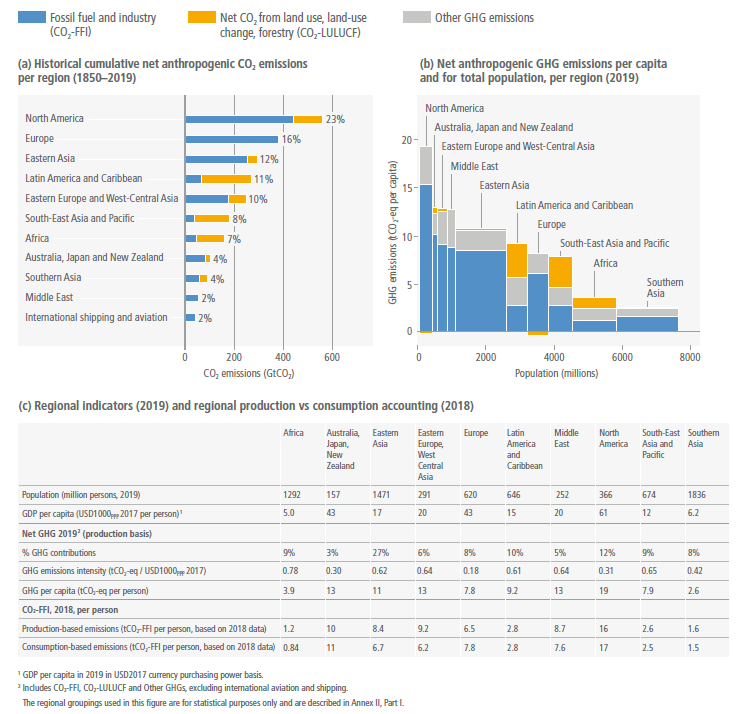

Territorial emissions from developing country regions continue to grow, mostly driven by increased consumption and investment, albeit starting from a low base of per-capita emissions and with a lower historic contribution to cumulative emissions than developed countries (high confidence). Average 2019 per-capita CO2-FFI emissions in three developing regions, Africa (1.2 tCO2), Asia and Pacific (4.4 tCO2), and Latin America and Caribbean (2.7 tCO2), remained less than half of Developed Countries’ 2019 CO2-FFI emissions (9.5 tCO2). In these three developing regions together, CO2-FFI emissions grew by 26% between 2010 and 2019 (compared to 260% between 1990 and 2010). In contrast, in Developed Countries emissions contracted by 9.9% between 2010 and 2019 and by 9.6% between 1990 and 2010. Historically, these three developing regions together contributed 28% to cumulative CO2-FFI emissions between 1850 and 2019, whereas Developed Countries contributed 57%, and least developed countries contributed 0.4%. (Figure TS.5) {2.2, Figures 2.9 and 2.10}

Figure TS.5 | Global emissions are distributed unevenly, both in the present day and cumulatively since 1850. Panel (a) shows the distribution of regional GHG emissions in tonnes CO2-eq per capita by region in 2019. GHG emissions are categorised into: CO2 fossil fuel and industry (CO2-FFI); CO2 land use, land-use change and forestry (CO2-LULUCF); and other GHG emissions (CH4, nitrous oxide, F-gas, expressed in CO2-eq using GWP100). The height of each rectangle shows per-capita emissions, the width shows the population of the region, so that the area of the rectangles refers to the total emissions for each regional. Percentages refer to overall GHG contributions to total global emissions in 2019. Emissions from international aviation and shipping are not included. Panel (b) shows the share of historical net CO2 emissions per region from 1850 to 2019. This includes CO2-FFI and CO2-LULUCF (GtCO2). Other GHG emissions are not included. Emissions from international aviation and shipping are included. Panel (c) shows population, GDP per person, emission indicators by region in 2019 for percentage GHG contributions, total GHG per person, and total GHG emissions intensity, together with production-based and consumption-based CO2-FFI data, which is assessed in this report up to 2018. Consumption-based emissions are emissions released to the atmosphere in order to generate the goods and services consumed by a certain entity (e.g., region). Emissions from international aviation and shipping are not included. {1.3, Figure 1.2a, 2.2, Figure 2.10}

Globally, households with income in the top 10% contribute about 36–45% of global GHG emissions (robust evidence, medium agreement). About two thirds of the top 10% live in Developed Countries and one third in other economies. The lifestyle consumption emissions of the middle income and poorest citizens in emerging economies are between five and 50 times below their counterparts in high-income countries (medium confidence). Increasing inequality within a country can exacerbate dilemmas of redistribution and social cohesion, and affect the willingness of the rich and poor to accept policies to protect the environment, and to accept and afford lifestyle changes that favour mitigation (medium confidence). {2.6.1, 2.6.2, Figure 2.29}

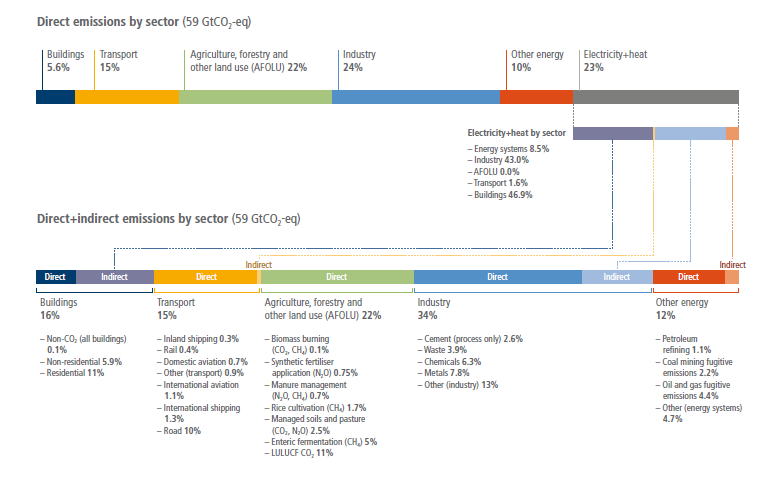

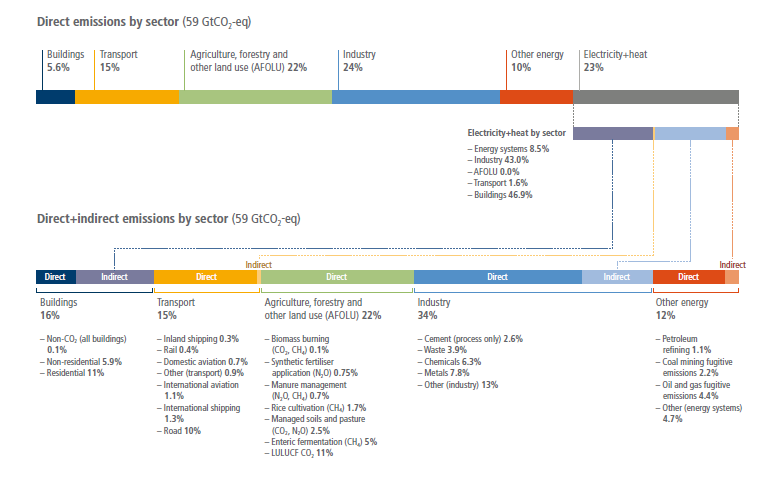

Globally, GHG emissions continued to rise across all sectors and subsectors, and most rapidly in transport and industry (high confidence). In 2019, 34% (20 GtCO2-eq) of global GHG emissions came from the energy sector, 24% (14 GtCO2-eq) from industry, 22% (13 GtCO2-eq) from agriculture, forestry and other land use (AFOLU), 15% (8.7 GtCO2-eq) from transport, and 5.6% (3.3 GtCO2-eq) from buildings. Once indirect emissions from energy use are considered, the relative shares of industry and buildings emissions rise to 34% and 16%, respectively. Average annual GHG emissions growth during 2010–2019 slowed compared to the previous decade in energy supply (from 2.3% to 1.0%) and industry (from 3.4% to 1.4%, direct emissions only), but remained roughly constant at about 2% yr –1 in the transport sector ( high confidence). Emission growth in AFOLU is more uncertain due to the high share of CO2-LULUCF emissions (medium confidence). (Figure TS.8) {2.2.4, Figure 2.13 and Figures 2.16–2.21}

There is a discrepancy, equating to 5.5 GtCO2yr–1, between alternative methods of accounting for anthropogenic land CO2fluxes. Accounting for this discrepancy would assist in assessing collective progress in a global stocktake (high confidence). The principal accounting approaches are national GHG inventories (NGHGI) and global modelling 11 approaches. NGHGI, based on IPCC guidelines, consider a much larger area of forest to be under human management than global models. NGHGI consider the fluxes due to human-induced environmental change on this area to be anthropogenic and are thus reported. Global models, in contrast, consider these fluxes to be natural and are excluded from the total reported anthropogenic land CO2 flux. The accounting method used will affect the assessment of collective progress in a global stocktake (medium confidence) {Cross-Chapter Box 6 in Chapter 7}. In the absence of these adjustments, allowing a like-with-like comparison, collective progress would appear better than it is. {7.2}

This accounting discrepancy also applies to Integrated Assessment Models (IAMs), with the consequence that anthropogenic land CO2fluxes reported in IAM pathways cannot be compared directly with those reported in national GHG inventories (high confidence). Methodologies enabling a more like-for-like comparison between models’ and countries’ approaches would support more accurate assessment of the collective progress achieved under the Paris Agreement. {3.4, 7.2.2}

Average annual growth in GHG emissions from energy supply decreased from 2.3% for 2000–2009 to 1.0% for 2010–2019 (high confidence). This slowing of growth is attributable to further improvements in energy efficiency and reductions in the carbon intensity of energy supply driven by fuel switching from coal to gas, reduced expansion of coal capacity, particularly in Eastern Asia, and the increased use of renewables (medium confidence). (Figure TS.6) {2.2.4, 2.4.2.1, Figure 2.17}

The industry, buildings and transport sectors make up 44% of global GHG emissions, or 66% when the emissions from electricity and heat production are reallocated asindirect emissions (high confidence). This reallocation makes a substantial difference to overall industry and buildings emissions as shown in Figure TS.6. Industry, buildings, and transport emissions are driven, respectively, by the large rise in demand for basic materials and manufactured products, a global trend of increasing floor space per capita, building energy service use, travel distances, and vehicle size and weight. Between 2010 and 2019, aviation grew particularly fast on average at about 3.3% per annum. Globally, energy efficiency has improved in all three demand sectors, but carbon intensities have not. (Figure TS.6) {2.2.4, Figures 2.18, 2.19 and 2.20}

Figure TS.6 | Total anthropogenic direct and indirect GHG emissions for the year 2019 (in GtCO2-eq) by sector and subsector. Direct emissions estimates assign emissions to the sector in which they arise (scope 1 reporting). Indirect emissions – as used here – refer to the reallocation of emissions from electricity and heat to the sector of final use (scope 2 reporting). Note that cement refers to process emissions only, as a lack of data prevents the full reallocation of indirect emissions to this sector. More comprehensive conceptualisations of indirect emissions including all products and services (scope 3 reporting) are discussed in Section 2.3. Emissions are converted into CO2-equivalents based on global warming potentials with a 100-year time horizon (GWP100) from the IPCC Sixth Assessment Report. Percentages may not add up to 100 across categories due to rounding at the second significant digit. {Figure 2.12, 2.3}

Providing access to modern energy services universally would increase global GHG emissions by a few percent at most (high confidence). The additional energy demand needed to support decent living standards12 for all is estimated to be well below current average energy consumption (medium evidence, high agreement ). More equitable income distribution could also reduce carbon emissions, but the nature of this relationship can vary by level of income and development (limited evidence, medium agreement ). {2.4.3}

Evidence of rapid energy transitions exists in some case studies (medium confidence). Emerging evidence since AR5 on past energy transitions identifies a growing number of cases of accelerated technology diffusion at sub-global scales and describes mechanisms by which future energy transitions may occur more quickly than those in the past. Important drivers include technology transfer and cooperation, international policy and financial support, and harnessing synergies among technologies within a sustainable energy system perspective (medium confidence). A fast global low-carbon energy transition enabled by finance to facilitate low-carbon technology adoption in developing and particularly in least developed countries can facilitate achieving climate stabilisation targets ( high confidence). {2.5.2, Table 2.5}

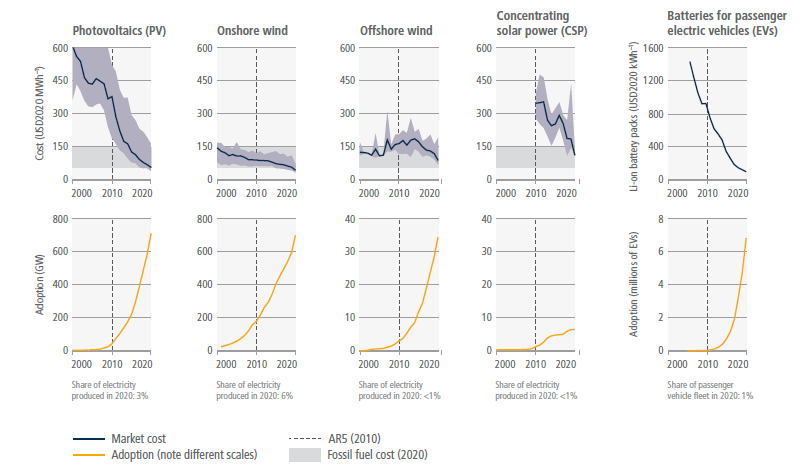

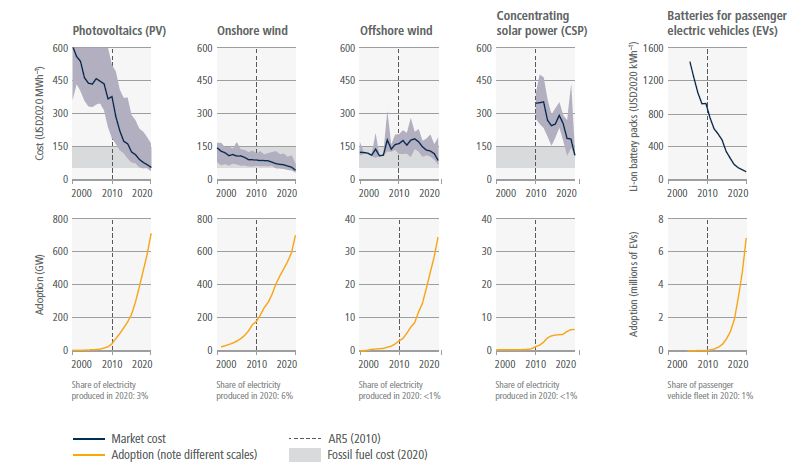

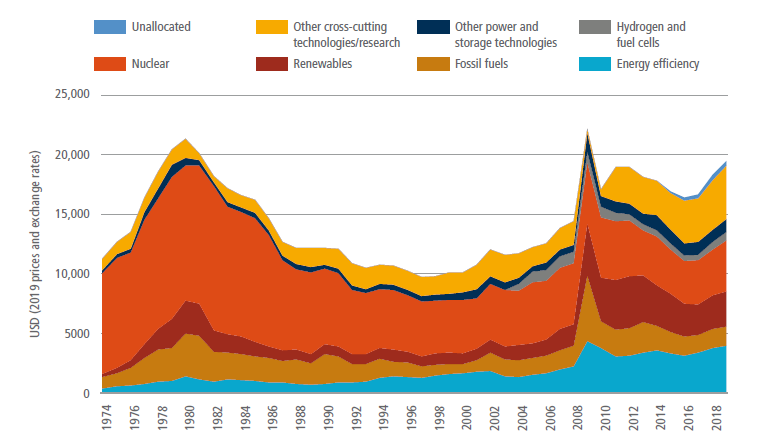

Multiple low-carbon technologies have shown rapid progress since AR5 – in cost, performance, and adoption – enhancing the feasibility of rapid energy transitions (high confidence). The rapid deployment and unit cost decrease of modular technologies like solar, wind, and batteries have occurred much faster than anticipated by experts and modelled in previous mitigation scenarios, as shown in Figure TS.7 ( high confidence). The political, economic, social, and technical feasibility of solar energy, wind energy and electricity storage technologies has improved dramatically over the past few years. In contrast, the adoption of nuclear energy and CO2 capture and storage (CCS) in the electricity sector has been slower than the growth rates anticipated in stabilisation scenarios. Emerging evidence since AR5 indicates that small-scale technologies (e.g., solar, batteries) tend to improve faster and be adopted more quickly than large-scale technologies (nuclear, CCS) (medium confidence). (Figure TS.7, Box TS.15) {2.5.3, 2.5.4, Figures 2.22 and 2.23}

Figure TS.7 | The unit costs of batteries and some forms of renewable energy have fallen significantly, and their adoption continues to increase. The top panel shows global costs per unit of energy (USD per MWh) for some rapidly changing mitigation technologies. Solid blue lines indicate average unit cost in each year. Light blue shaded areas show the range between the 5th and 95th percentiles in each year. Grey shading indicates the range of unit costs for new fossil fuel (coal and gas) power in 2020 (corresponding to USD55–148 per MWh). In 2020, the levelised costs of energy (LCOE) of the four renewable energy technologies could compete with fossil fuels in many places. For batteries, costs shown are for 1 kWh of battery storage capacity; for the others, costs are LCOE, which includes installation, capital, operations, and maintenance costs per MWh of electricity produced. The literature uses LCOE because it allows consistent comparisons of cost trends across a diverse set of energy technologies to be made. However, it does not include the costs of grid integration or climate impacts. Further, LCOE does not take into account other environmental and social externalities that may modify the overall (monetary and non-monetary) costs of technologies and alter their deployment. The bottom panel shows cumulative global adoption for each technology, in GW of installed capacity for renewable energy and in millions of vehicles for battery-electric vehicles. A vertical dashed line is placed in 2010 to indicate the change since AR5. Shares of electricity produced and share of passenger vehicle fleet are indicated in text for 2020 based on provisional data, i.e., percentage of total electricity production (for PV, onshore wind, offshore wind, CSP) and of total stock of passenger vehicles (for EVs). The electricity production share reflects different capacity factors; for example, for the same amount of installed capacity, wind produces about twice as much electricity as solar PV. {2.5, 6.4} Renewable energy and battery technologies were selected as illustrative examples because they have recently shown rapid changes in costs and adoption, and because consistent data are available. Other mitigation options assessed in the report are not included as they do not meet these criteria.

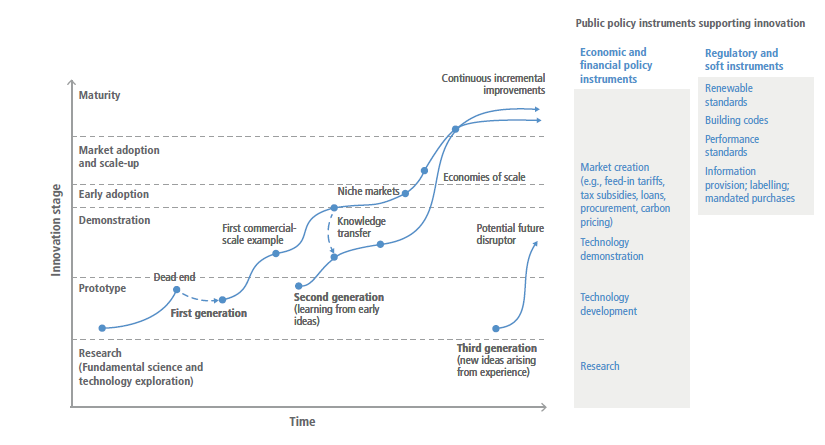

Robust incentives for investment in innovation, especially incentives reinforced by national policy and international agreements, are central to accelerating low-carbon technological change (robust evidence, medium agreement). Policies have driven innovation, including instruments for technology push (e.g., scientific training, research and development (R&D)) and demand pull (e.g., carbon pricing, adoption subsidies), as well as those promoting knowledge flows and especially technology transfer. The magnitude of the scale-up challenge elevates the importance of rapid technology development and adoption. This includes ensuring participation of developing countries in an enhanced global flow of knowledge, skills, experience, equipment, and technology; which in turn requires strong financial, institutional, and capacity-building support. {16.4, 16.5}

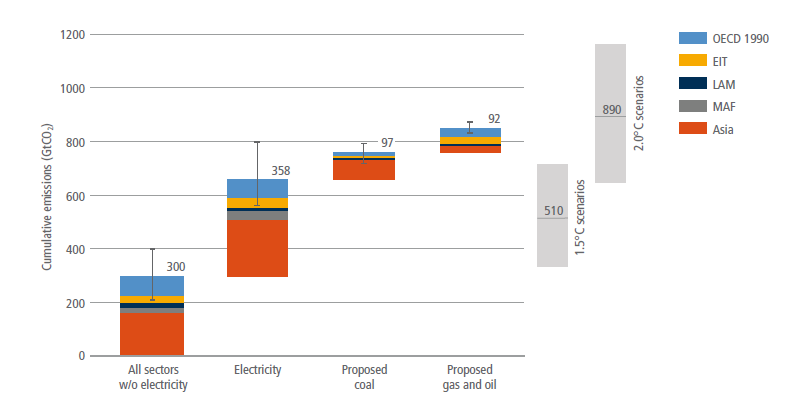

Estimates of future CO2 emissions from existing fossil fuel infrastructures already exceed remaining cumulative net CO2 emissions in pathways limiting warming to 1.5°C (>50%) with no or limited overshoot (high confidence). Assuming variations in historic patterns of use and decommissioning, estimated future CO2 emissions from existing fossil fuel infrastructure alone are 660 (460–890) GtCO2 and from existing and currently planned infrastructure 850 (600–1100) GtCO2. This compares to overall cumulative net CO2 emissions until reaching net zero CO2 of 510 (330–710) GtCO2 in pathways that limit warming to 1.5°C (>50%) with no or limited overshoot, and 890 (640–1160) GtCO2 in pathways that limit warming to 2°C (>67%) ( high confidence). While most future CO2 emissions from existing and currently planned fossil fuel infrastructure are situated in the power sector, most remaining fossil fuel CO2 emissions in pathways that limit warming to 2°C (>67%) and below are from non-electric energy – most importantly from the industry and transportation sectors ( high confidence). Decommissioning and reduced utilisation of existing fossil fuel installations in the power sector as well as cancellation of new installations are required to align future CO2 emissions from the power sector with projections in these pathways ( high confidence). (Figure TS.8) {2.7.2, 2.7.3, Figure 2.26, Tables 2.6 and 2.7}

Figure TS.8 | Future CO2 emissions from existing and currently planned fossil fuel infrastructure in the context of the Paris Agreement carbon budgets in GtCO2based on historic patterns of infrastructure lifetimes and Future CO2 emissions estimates of existing infrastructure for the electricity sector as well as all other sectors (industry, transport, buildings, other fossil fuel infrastructures) and of proposed infrastructures for coal power as well as gas and oil power. Grey bars on the right depict the range (5–95th percentile) in overall cumulative net CO2 emissions until reaching net zero CO2 in pathways that limit warming to 1.5°C (>50%) with no or limited overshoot (1.5°C scenarios), and in pathways that limit warming to 2°C (>67%) (2°C scenarios). {Figure 2.26}

TS.4 Mitigation and Development Pathways

While previous WGIII assessments have explored mitigation pathways, since AR5 there has been an increasing emphasis in the literature on development pathways, and in particular at the national scale. Chapter 4 assesses near-term (2019–2030) to mid-term (2030–2050) pathways, complementing Chapter 3 which focuses on long-term pathways (up to 2100). While there is considerable literature on country-level mitigation pathways, including but not limited to NDCs, the country distribution of this literature is very unequal ( high confidence). {4.2.1, Cross-Chapter Box 4 in Chapter 4}

TS.4.1 Mitigation and Development Pathways in the Near- to Mid-term

An emissions gap persists, exacerbated by an implementation gap, despite mitigation efforts including those in Nationally Determined Contributions (NDCs). In this report the emissions gap is understood as the difference between projected global emissions with Nationally Determined Contributions (NDCs) in 2030, and emissions in 2030 if mitigation pathways consistent with the Paris temperature goals were achieved. The term implementation gap refers to the gap between NDC mitigation pledges and the expected outcome of existing policies.

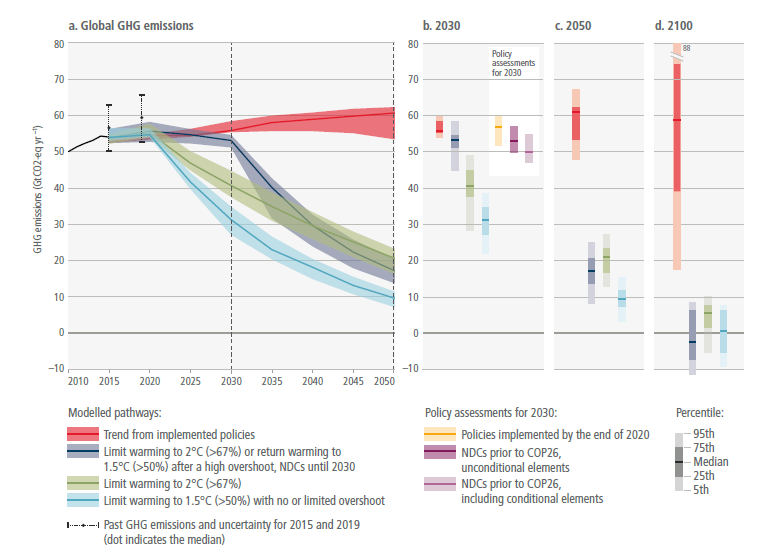

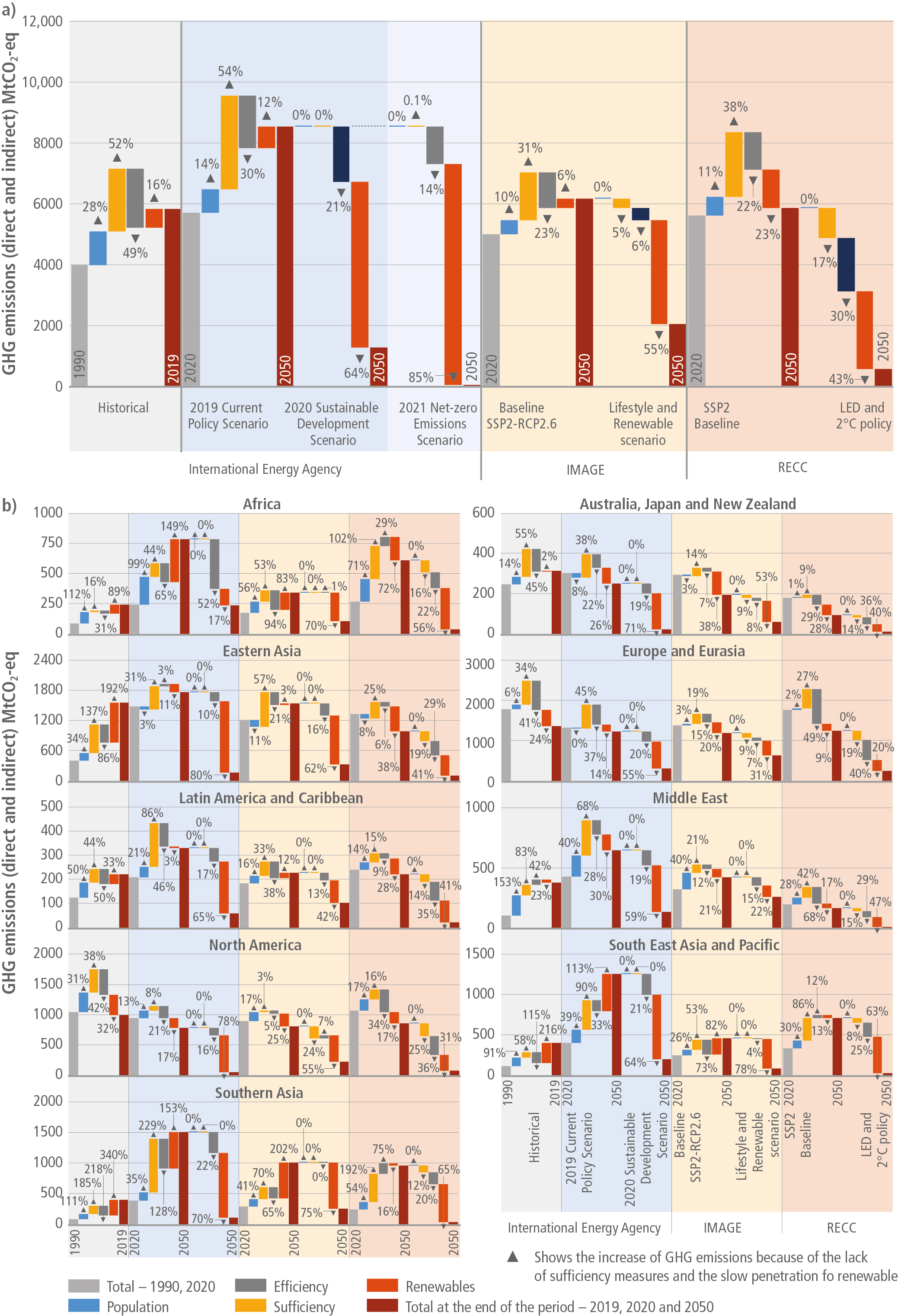

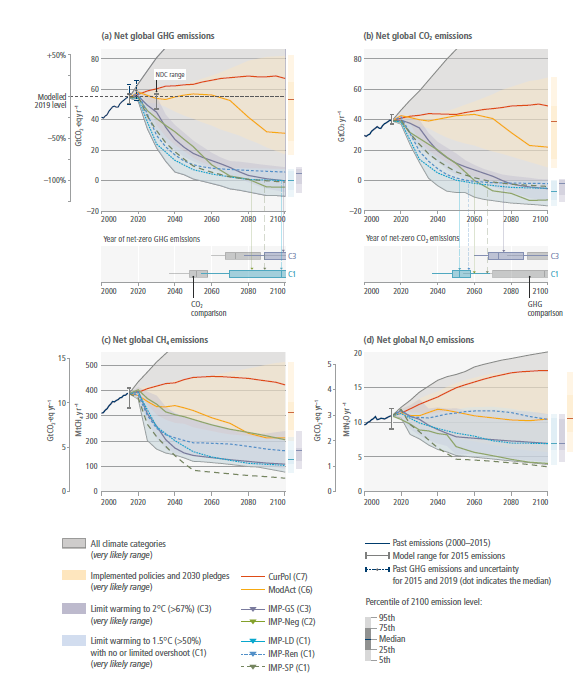

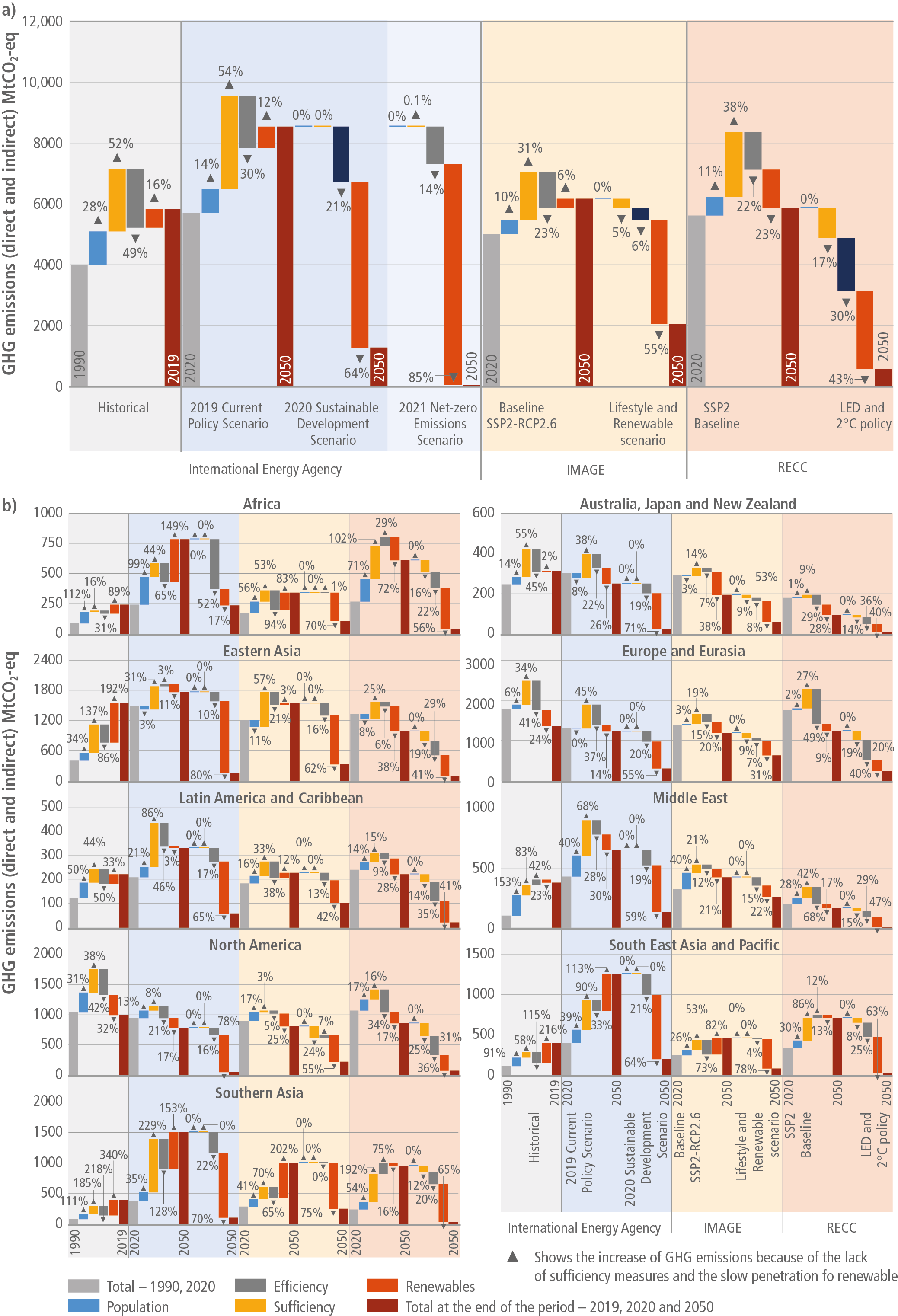

Pathways consistent with the implementation and extrapolation of countries’ current 13 policies see GHG emissions reaching 57 (52–60) GtCO2-eq yr–1by 2030 and to 46–67 GtCO2-eq yr–1by 2050, leading to a median global warming of 2.4°C to 3.5°C by 2100 (medium confidence). NDCs with unconditional and conditional elements 14 lead to 53 (50–57) and 50 (47–55) GtCO2-eq, respectively (medium confidence) {Table 4.1}. This leaves median estimated emissions gaps of 14–23 GtCO2-eq to limit warming to 2°C and 25–34 GtCO2-eq to limit warming to 1.5°C relative to mitigation pathways. (Figure TS.9) {Cross-Chapter Box 4, Figure 1 in Chapter 4}

Figure TS.9 | Aggregate greenhouse gas (GHG) emissions of global mitigation pathways (coloured funnels and bars) and projected emission outcomes from current policies and emissions implied by unconditional and conditional elements of NDCs, based on updates available by 11 October 2021 (grey bars). Shaded areas show GHG emission medians and 25–75th percentiles over 2020–2050 for four types of pathways in the AR6 scenario database: (i) pathways with near-term emissions developments in line with current policies and extended with comparable ambition levels beyond 2030; (ii) pathways likely to limit warming to 2°C with near-term emissions developments reflecting 2030 emissions implied by current NDCs followed by accelerated emissions reductions; (iii) pathways likely to limit warming to 2°C based on immediate actions from 2020 onwards; (iv) pathways that limit warming to 1.5°C with no or limited overshoot. Right-hand panels show two snapshots of the 2030 and 2050 emission ranges of the pathways in detail (median, 25–75th and 5–95th percentiles). The 2030 snapshot includes the projected emissions from the implementation of the NDCs as assessed in Section 4.2 (Table 4.1; median and full range). Historic GHG emissions trends as used in model studies are shown for 2010–2015. GHG emissions are in CO2-equivalent using GWP100 values from AR6. {3.5, Table 4.1, Cross-Chapter Box 4 in Chapter 4}

Projected global emissions from aggregated NDCs place limiting global warming to 1.5°C beyond reach and make it harder after 2030 to limit warming to 2°C (high confidence). Pathways following NDCs until 2030 show a smaller reduction in fossil fuel use, slower deployment of low-carbon alternatives, and a smaller reduction in CO2, CH4 and overall GHG emissions in 2030 compared to immediate action scenarios. This is followed by a much faster reduction of emissions and fossil fuels after 2030, and a larger increase in the deployment of low-carbon alternatives during the medium term in order to get close to the levels of the immediate action pathways in 2050. Those pathways also deploy a larger amount of carbon dioxide removal (CDR) to compensate for higher emissions before 2030. The faster transition during 2030 to 2050 entails greater investment in fossil fuel infrastructure and lower deployment of low-carbon alternatives in 2030, which adds to the socio-economic challenges in realising the higher transition rates. (TS.4.2) {3.5}

Studies evaluating up to 105 updated NDCs15 indicate that emissions in NDCs with conditional elements have been reduced by 4.5 (2.7–6.3) GtCO2-eq. This closes the emission gaps by about one third to 2°C and about 20% to 1.5°C compared to the original NDCs submitted in 2015/16 (medium confidence) {4.2.2, Cross-Chapter Box 4 in Chapter 4}. An implementation gap also exists between the projected emissions with ‘current policies’ and the projected emissions resulting from the implementation of the unconditional and conditional elements of NDCs; this is estimated to be around 4 and 7 GtCO2-eq in 2030, respectively (medium confidence) {4.2.2}. Many countries would therefore require additional policies and associated action on climate change to meet their autonomously determined mitigation targets as specified under the first NDCs (limited evidence). The disruptions triggered by the COVID-19 pandemic increase uncertainty over the range of projections relative to pre-COVID-19 literature. As indicated by a growing number of studies at the national and global level, how large near- to mid-term emissions implications of the COVID-19 pandemic are, to a large degree depends on how stimulus or recovery packages are designed. {4.2}

There is a need to explore how accelerated mitigation – relative to NDCs and current policies – could close both emission gaps and implementation gaps. There is increasing understanding of the technical content of accelerated mitigation pathways, differentiated by national circumstances, with considerable, though uneven, literature at country-level (medium evidence, high agreement ). Transformative technological and institutional changes for the near term include demand reductions through efficiency and reduced activity, rapid decarbonisation of the electricity sector and low-carbon electrification of buildings, industry and transport (robust evidence, medium agreement ). A focus on energy use and supply is essential, but not sufficient on its own – the land sector and food systems deserve attention. The literature does not adequately include demand-side options and systems analysis, and captures the impact from non-CO2GHGs (medium confidence). {4.2.5}

If obstacles to accelerated mitigation are rooted in underlying structural features of society, then transforming such structures can support emission reductions {4.2.6}. Countries and regions will have different starting points for transition pathways. Some critical differences between countries include climate conditions resulting in different heating and cooling needs, endowments with different energy resources, patterns of spatial development, and political and economic conditions {4.2.5}. The way countries develop determines their capacity to accelerate mitigation and achieve other sustainable development objectives simultaneously (medium confidence){4.3.1, 4.3.2}. Yet meeting ambitious mitigation and development goals cannot be achieved through incremental change (robust evidence, medium agreement ). Though development pathways result from the actions of a wide range of actors, it is possible to shift development pathways through policies and enhancing enabling conditions (limited evidence, medium agreement ).

Shifting development pathways towards sustainabilityoffers ways to broaden the range of levers and enablers that a society can use to accelerate mitigation and increases the likelihood of making progress simultaneously on climate action and other development goals (Box TS.3) {Cross-Chapter Box 5 in Chapter 4, Figure 4.7, 4.3}. There are practical options to shift development pathways in ways that advance mitigation and other sustainable development objectives, support political feasibility, increase resources to meet multiple goals, and reduce emissions (limited evidence, high agreement ). Concrete examples, assessed in Chapter 4 of this report, include high-employment and low-emissions structural change; fiscal reforms for mitigation and social contract, combining housing policies to deliver both housing and transport mitigation; and changed economic, social and spatial patterns of agriculture sector development, providing the basis for sustained reductions in emissions from deforestation. {4.4.1, 4.4, 1.10}

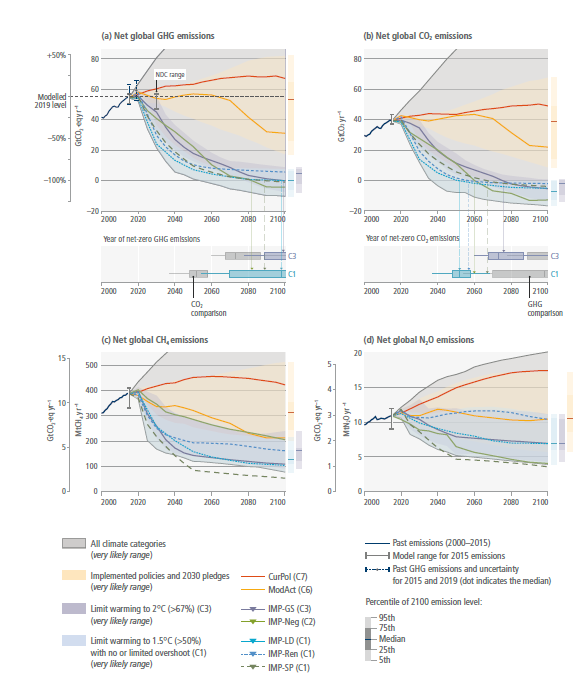

Table TS. 2 | Comparison of key characteristics of mitigation pathways with immediate action towards limiting warming to 1.5-2°C vs. pathways following NDCs announced prior to COP26 until 2030. Key characteristics are reported for five groups of mitigation pathways: (i) immediate action to limit warming to 1.5°C (>50%) with no or limited overshoot (C1 in Table TS.3; 97 scenarios), (ii) near term action following the NDCs until 2030 and returning warming to 1.5°C (> 50%) by 2100 after a high overshoot (subset of 42 scenarios following the NDCs until 2030 in C2), (iii) immediate action to limit warming to 2°C (>67%), (C3a in Table TS.3; 204 scenarios), (iv) near term action following the NDCs until 2030 followed by post-2030 action to limit warming to 2°C (>67%) (C3b in Table TS.3; 97 scenarios). Also shown are the characteristics for (v) the combined class of all scenarios that limit warming to 2°C (>67%). The groups (i), (iii), and the combination of (ii) and (iv) are depicted in Figure TS.9. Reported are median and interquartile ranges (in brackets) for selected global indicators. Numbers are rounded to the nearest five, with the exception of cumulative net negative CO2 emissions rounded to the nearest 10. Changes from 2019 are relative to modelled 2019 values. Emissions reductions are based on harmonised model emissions used for the climate assessment. {Section 3.5} {Table 3.6}

Global indicators | 1.5°C (>50%) | 1.5°C (>50%) by 2100 | 2°C (>67%) | ||

Immediate action, with no or limited overshoot | NDCs until 2030, with overshoot before 2100 | Immediate action | NDCs until 2030 | All | |

Cumulative net negative CO2 emissions until 2100 (GtCO2) | 220 (70,430) | 380 (300,470) | 30 (0,130) | 60 (20,210) | 40 (10,180) |

Change in GHG emissions in 2030 (% rel to 2019) | –45 (–50,–40) | –5 (–5,0) | –25 (–35,–20) | –5 (–10,0) | –20 (–30,–10) |

in 2050 (% rel to 2019) | –85 (–90,–80) | –75 (–85,–70) | –65 (–70,–60) | –70 (–70,–60) | –65 (–70,–60) |

Change in CO2 emissions in 2030 (% rel to 2019) | –50 (–60,–40) | –5 (–5,0) | –25 (–35,–20) | –5 (–5,0) | –20 (–30,–5) |

in 2050 (% rel to 2019) | –100 (–105,–95) | –85 (–95,–80) | –70 (–80,–65) | –75 (–80,–65) | –75 (–80,–65) |

Change in net land use CO2 emissions in 2030 (% rel to 2019) | –100 (–105,–95) | –30 (–60,–20) | –90 (–105,–75) | –20 (–80,–20) | –80 (–100,–30) |

in 2050 (% rel to 2019) | –150 (–200,–100) | –135 (–165,–120) | –135 (–185,–100) | –130 (–145,–115) | –135 (–180,–100) |

Change in CH4 emissions in 2030 (% rel to 2019) | –35 (–40,–30) | –5 (–5,0) | –25 (–35,–20) | –10 (–15,–5) | –20 (–25,–10) |

in 2050 (% rel to 2019) | –50 (–60,–45) | –50 (–60,–45) | –45 (–50,–40) | –50 (–65,–45) | –45 (–55,–40) |

Change in primary energy from coal in 2030 (% rel to 2019) | –75 (–80,–65) | –10 (–20,–5) | –50 (–65,–35) | –15 (–20,–10) | –35 (–55,–20) |

in 2050 (% rel to 2019) | –95 (–100,–80) | –90 (–100,–85) | –85 (–100,–65) | –80 (–90,–70) | –85 (–95,–65) |

Change in primary energy from oil in 2030 (% rel to 2019) | –10 (–25,0) | 5 (5,10) | 0 (–10,10) | 10 (5,10) | 5 (0,10) |

in 2050 (% rel to 2019) | –60 (–75,–40) | –50 (–65,–35) | –30 (–45,–15) | –40 (–55,–20) | –30 (–50,–15) |

Change in primary energy from gas in 2030 (% rel to 2019) | –10 (–30,0) | 15 (10,25) | 10 (0,15) | 15 (10,15) | 10 (0,15) |

in 2050 (% rel to 2019) | –45 (–60,–20) | –45 (–55,–30) | –10 (–35,15) | –30 (–45,–5) | –15 (–40,10) |

Change in primary energy from nuclear in 2030 (% rel to 2019) | 40 (10,70) | 10 (0,25) | 35 (5,50) | 10 (0,30) | 25 (0,45) |

in 2050 (% rel to 2019) | 90 (15,295) | 100 (45,130) | 85 (30,200) | 75 (30,120) | 80 (30,140) |

Change in primary energy from modern biomass in 2030 (% rel to 2019) | 75 (55,130) | 45 (20,75) | 60 (35,105) | 45 (20,80) | 55 (35,105) |

in 2050 (% rel to 2019) | 290 (215,430) | 230 (170,420) | 240 (130,355) | 260 (95,435) | 250 (115,405) |

Change in primary energy from non-biomass renewables in 2030 (% rel to 2019) | 225 (155,270) | 100 (85,145) | 150 (115,190) | 115 (85,130) | 130 (90,170) |

in 2050 (% rel to 2019) | 725 (545,950) | 665 (535,925) | 565 (415,765) | 625 (545,700) | 605 (470,735) |

Change in carbon intensity of electricity in 2030 (% rel to 2019) | –75 (–80,–70) | –30 (–40,–30) | –60 (–70,–50) | –35 (–40,–30) | –50 (–65,–35) |

in 2050 (% rel to 2019) | –100 (–100,–100) | –100 (–100,–100) | –95 (–100,–95) | –100 (–100,–95) | –95 (–100,–95) |

Box TS.3 | Shifting Development Pathways to Increase Sustainability and Broaden Mitigation Options

In this report, development pathways refer to the patterns of development resulting from multiple decisions and choices made by many actors in the national and global contexts. Each society whether in developing or developed regions follows its own pattern of growth (Figure TS.13). Development pathways can also be described at smaller scales (e.g., for regions or cities) and for sectoral systems.

Development pathways are major drivers of GHG emissions {1, 2}. There is compelling evidence to show that continuing along existing development pathways will not achieve rapid and deep emission reductions. In the absence of shifts in development pathways, conventional mitigation policy instruments may not be able to limit global emissions to a degree sufficient to meet ambitious mitigation goals or they may only be able to do so at very high economic and social costs.

Policies to shift development pathways, on the other hand, make mitigation policies more effective. Shifting development pathways broadens the scope for synergies between sustainable development objectives and mitigation. Development pathways also determine the enablers and levers available for adaptation {AR6 WGII TS.E.1.2} and for achieving other SDGs.

There are many instances in which reducing GHG emissions and moving towards the achievement of other development objectives can go hand in hand {Chapter 3, Figure 3.33, Chapters 6–12, and 17}. Integrated policies can support the creation of synergies between action to combat climate change and its impacts (SDG 13 – climate action) and other SDGs. For example, when measures promoting walkable urban areas are combined with electrification and clean renewable energy, there are several co-benefits to be attained. These include reduced pressures on agricultural land from reduced urban growth, health co-benefits from cleaner air, and benefits from enhanced mobility {8.2, 8.4, 4.4.1}. Energy efficiency in buildings and energy poverty alleviation through improved access to clean fuels also deliver significant health benefits. {9.8.1 and 9.8.2}

However, decisions about mitigation actions, and their timing and scale, may entail trade-offs with the achievement of other national development objectives in the near, mid- and long term {Chapter 12}. In the near term, for example, regulations may ban vehicles from city centres to reduce congestion and local air pollution but reduce mobility and choice. Increasing green spaces within cities without caps on housing prices may involve trade-offs with affordable housing and push low-income residents outside the city {8.2.2}. In the mid- and long term, large-scale deployment of biomass energy raises concerns about food security and biodiversity conservation {3.7.1, 3.7.5, 7.4.4, 9.8.1, 12.5.2, 12.5.3}. Prioritising is one way to manage these trade-offs, addressing some national development objectives earlier than others. Another way is to adopt policy packages aimed at shifting development pathways towards increased sustainability (SDPS) as they expand the range of tools available to simultaneously achieve multiple development objectives and accelerate mitigation. (Box TS.3, Figure 1)

What does shifting development pathways towards increased sustainability entail?

Shifting development pathways towards increased sustainability implies making transformative changes that disrupt existing developmental trends. Such choices would not be marginal, but include technological, systemic and socio-behavioural changes {4.4}. Decision points also arise with new infrastructure, sustainable supply chains, institutional capacities for evidence-based and integrated decision-making, financial alignment towards low-carbon socially responsible investments, just transitions and shifts in behaviour and norms to support shifts away from fossil fuel consumption. Adopting multi-level governance modes, tackling corruption where it inhibits shifts to sustainability, and improving social and political trust are also key for aligning and supporting long-term environmentally just policies and processes. {4.4, Cross-Chapter Box 5 in Chapter 4}

How can development pathways be ‘shifted’?